The Weekend Edition includes a market update plus Morningstar adds links to two highlights from the week.

Weekend market update

On Friday in the US, both the S&P500 and NASDAQ were flat, moving around 0.1%.

From AAP Netdesk: The Australian sharemarket gained ground for a fourth day in five sessions on Friday, although its early gains ebbed in the afternoon. The benchmark S&P/ASX200 index closed up 30 points on the day, or 0.5%, to 6,678. For the week, the index was up 2.1%, its best weekly performance since the week ending March 18. It's still down 10.3% for the year after an 8.9% selloff in June.

The energy sector led the market on Friday, climbing 2.1% after oil prices rebounded from a two-day sharp decline. Woodside Energy gained 1.7% and Santos climbed 2.3%. The materials sector closed Friday up 1.2%, with BHP adding 0.7% to $39.22, Rio Tinto up 0.3% and Fortescue up 0.6%. The big banks were down, with CBA falling 0.5% to $92.59 and ANZ dropping 0.4% to $27.70. Magellan Financial Group dipped 3% to $11.90 after the wealth manager reported $5.2 billion in net outflows during the June quarter, leaving it with $61.3 billion in funds under management. Tech stocks gained 0.8%, with Xero adding 1.6% and Dicker Data up 1.0%. The Australian dollar was buying 68.20 US cents.

From Shane Oliver, AMP Capital: Sharemarkets mostly rose over the last week on hopes that central banks will be able to tame inflation without causing a recession. However, it was messy with Eurozone shares – where the risk of recession is greatest – first making a new bear market low earlier in the week.

The beat goes on with rising interest rates but there was nothing really new over the last week. The minutes from the last Fed meeting were hawkish – referring to a “significant risk...[that] elevated inflation could become entrenched”, that the “outlook warranted moving to a restrictive stance” and that it saw a 50 or 75bps hike as being appropriate in July.

The hawkish pivot a month or so ago by central banks including the Reserve Bank has seen market expectations for longer-term inflation fall. Various indicators suggest that inflation pressures in the US may have peaked and if so this is positive sign for other countries including Australia as the US is leading other countries by about six months on inflation.

***

Into a new financial year, many thanks to over 700 retirees who completed our survey on their retirement experiences, including thousands of comments. We have split the results into two articles: the first gives tips on how to make the most of a retirement, and the second shows the full results of the survey including charts. With so many comments across nine questions, highly informative but too numerous to put in one article, Leisa Bell has summarised the results into a downloadable document. It's worth taking the time to scroll through them, I found them fascinating.

***

Behind the markets for last financial year delivering a fall in the S&P/ASX200 of 10% and a drop in the US S&P500 of nearly 20% lies every individual's personal experience. The US Treasury bond index lost 11%, offering none of the traditional bond protection. Even those who default into a balanced super fund will suffer their first negative returns since the GFC. Each investor must now decide whether to sit on their portfolio, sell to avoid further falls or invest more in bargain opportunities.

Howard Marks recently spoke about current market conditions on a Goldman Sachs podcast, saying:

“First of all, what is risk? It's the probability of a negative event in the future. What do we know about that? What does the past tell us about that? The past has relevance, but it's not absolute. I don't think risk can be measured. I don't think the past is absolutely applicable. In fact, the big money is lost at the juncture when the past stops being applicable, which happens eventually."

The last six months feels like one of those junctures. We learn from the past but we are guessing about the future. Mark Delaney, CIO at Australia's biggest super fund, AustralianSuper, released a statement explaining a loss of 2.7% in its main balanced fund for last financial year. The same option was up 20.4% the previous year and 9.3% per annum in the last decade, a period of excellent returns for default super fund investors. It will be a long time before another decade is as good.

Delaney said of the results:

"After more than 10 years of economic growth our outlook suggests a possible shift from economic expansion to slowdown in the coming years. In response, we have started to readjust to a more defensive strategy, as conditions become less supportive of growth asset classes such as shares."

He's a bit late to the game if he has just "started to readjust" as the signs were there in late 2021, as described in our editorials.

We all have different risk appetites and ways to think about investing. I have a friend who I've known for 40 years and he's been consistent in his strategy. He cares only about the income from his portfolio, and this is far less volatile than share prices. When CIMIC (formerly Leighton) was recently fully acquired by its German owner, he received a large cash payment which he wants to reinvest. What's his reaction to the recent sell off? "Shares are for sale at a discount. It's fantastic," he told me last week.

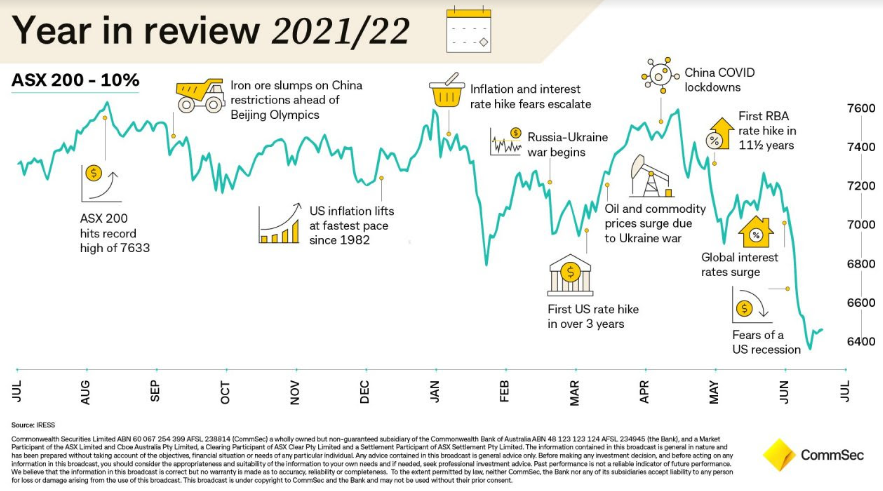

Most investors nursing losses are not so happy, and this neat graphic from CommSec shows how the year unfolded to deliver the 10% loss in the ASX200. It highlights how poorly the year ended.

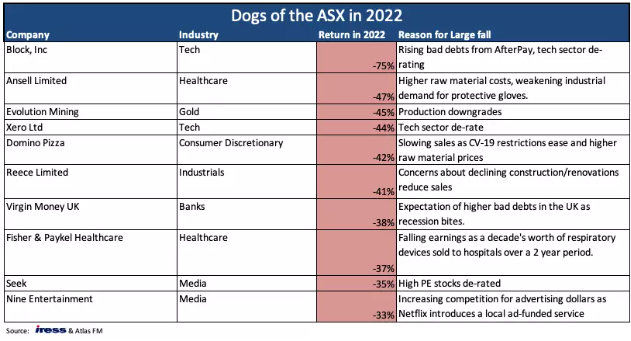

Hugh Dive of Atlas records the Dogs of the ASX each year, and here are the major losers. Wasn't everyone wearing gloves (Ansell), buying respiratory aids (Fisher & Paykel Healthcare) and buying pizza (Domino's) in the pandemic? AfterPay and BNPL rivals were replacing credit cards, Xero was driving business efficiency, job search was moving to Seek, Reece was riding the property boom. Hard to imagine anyone picked these 10 dogs during 2021.

The first-time, often younger, investors who jumped into the market in 2021 without the gains from prior years have found investing is difficult. It seemed like easy pickings when everything was up, from tech, Bitcoin, BNPL, online retail, NFTs, property. Interest rates lower than we'll ever see again pushed up the price of everything, and newbies bought on every tip in town. Now, late entrants to the greatest companies in the world are watching the red numbers with Amazon off 35% and Alphabet 22% in the June quarter.

For example, some tech-themed ETFs launched in Australia during the hype were ETFS Semiconductor (SEMI), down 33% last FY, BetaShares Crypto Innovators (CRYP) down 71% and Cosmos Global Digital Miners (DIGA), down 76%.

The debate is whether the losses suffered by younger people with a few thousand invested matters to them over the long term, as it is part of an investing journey and they have not lost much in dollar terms. Rob Arnott and Research Affiliates hold a view that is counter to traditional advice about risk appetite by age.

" ... we are told that the young are tolerant of risk and that, as retirement approaches, the average investor becomes intolerant of downside risk, fleeing after a serious drawdown ... Conventional wisdom suggests a percentage allocation to equities which is '100 minus your age' and the notion that the young can bear more risk than those of us who are middle aged (or older!). True, the young have more time to recover losses, but what losses are more insidious for retirees than inflation sapping the real income of a bond centric portfolio?

If young workers have to deal with their volatile young human capital over a long horizon - with a heightened need to cash out when the portfolio values are depressed - then it makes even more sense for younger workers to begin with a less risky portfolio. This also helps shape their risk tolerance so that their attitudes about investing and riskbearing are not poisoned by a bad early experience."

It's not a conventional view and bonds have not performed the protective role Arnott is writing about, but it's a legitimate challenge to the argument that equity exposure should reduce with age. Certainly, my mate, now in his 70s and fully exposed to equities, does not follow convention.

Our articles take the discussion further.

In this week's interview, Chris Demasi presents the case for ignoring short-term market falls when great long-term compounders are available at fair prices. This is not an argument to invest in just anything but the Amazons, Microsofts and Alphabets of the world that have strong future earnings. And he includes an Australian company in his portfolio.

Marcus Padley says investors should embrace the opportunities that come with fear in the market, and he describes five steps he has gone through in the recent selloff to decide the best way to respond.

Then Ian Rogers chronicles the end of Volt Bank, which was one of the challenger banks that seemed more likely to survive. Volt did not fail due bad loans, but the current predicament facing many startups as capital becomes harder to access. It shows the benefits of scale of the majors and the difficult regulatory environment for new players.

Campbell Harvey and Rob Arnott paint a concerning picture of the US economy. They write that the Fed was late to the game, inflation is likely to keep rising and the result of the Fed’s belated actions may push the economy into a recession.

Michael Collins explores how privacy-focused regulatory scrutiny is challenging the online-ad business that is built on the collection and dissemination of consumer data.

Morningstar tackled the increasing fears of a recession as Nicola Chand looks at Aussie miners after a commodities slump and Lewis Jackson checks why so many short sellers have descended on lithium miners.

The Reserve Bank decision this week to increase the cash rate by 0.5% to 1.35% comes with the expectation of another increase next month. The decision was justified by high global inflation - boosted by supply chain restrictions and the war in Ukraine - strong demand for goods, a tight labour market and capacity constraints. But Philip Lowe expects inflation to peak late in 2022 and decline back to the 2–3% range in 2023. His comments sounded slightly more relaxed about the need for future rate rises.

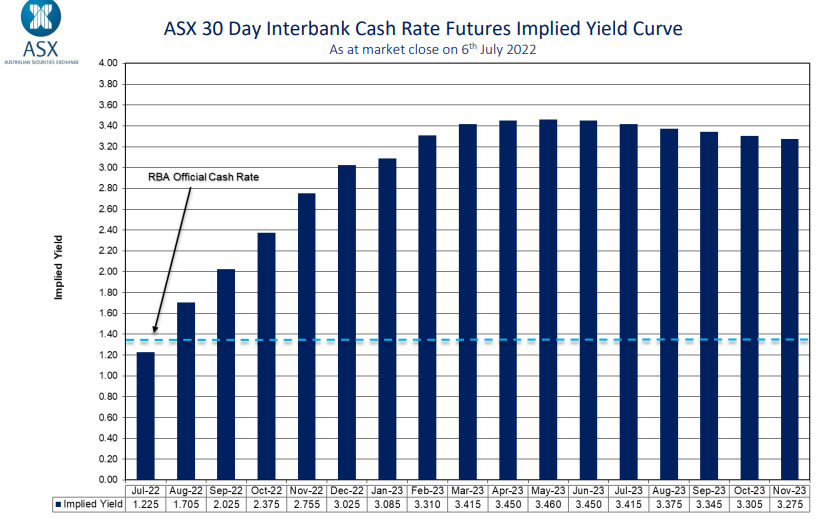

Where do we stand now? We have featured this ASX chart several times over recent months, and close watchers will see a significant fall in cash rate expectations. The implied rate for early 2023 is 3.4% but it was over 4% in mid-June, a level we said was highly improbable. It still looks too high, requiring a hefty 1.55% of further increases for the rest of 2022. Lowe does not want to see what that would do to property prices.

Graham Hand

Latest updates

PDF version of Firstlinks Newsletter

IAM Capital Markets' Weekly Market Insight

ASX Listed Bond and Hybrid rate sheet from NAB/nabtrade

Indicative Listed Investment Company (LIC) NTA Report from Bell Potter

LIC (LMI) Monthly Review from Independent Investment Research

Plus updates and announcements on the Sponsor Noticeboard on our website