The Weekend Edition includes a market update plus Morningstar adds links to two additional articles.

One of the bigger furphies in the funds industry is that portfolio managers must invest all their personal wealth in their own fund to 'align their interests' with their clients. It is supposed to ensure they work longer hours, turn over more stones, travel the world looking for the best companies and avoid the 'spend more time with the family' syndrome.

More accurate is that every fund manager is desperate for their fund to perform well, and putting 100% of their wealth in one strategy is poor asset allocation and likely to lead to more sleepless nights and worse personal relationships than are good for anyone's physical and mental health, and the fund's performance.

Next time this mantra is espoused by a fund manager, ask these questions:

"How is your performance improved by you holding nearly all your wealth in your fund? Will you work harder and better? Should I feel reassured when my $100,000 in your fund falls to $80,000 but your $5 million falls to $4 million? Why does it make sense for your wealth to be invested in your volatile small company fund?"

Funds management looks like (and often is) a glamorous job but every day is a competition against similarly-talented and driven people, both inside and outside their own firm. Imagine what happens when an analyst spends a month researching a company and deciding it is a strong buy, then after pitching the idea to colleagues, the proposal is rejected. It can feel like a takedown on a professional judgement. If a stock idea is rejected and then it rises strongly, everyone in the office knows and bonuses and pay increases may be hit.

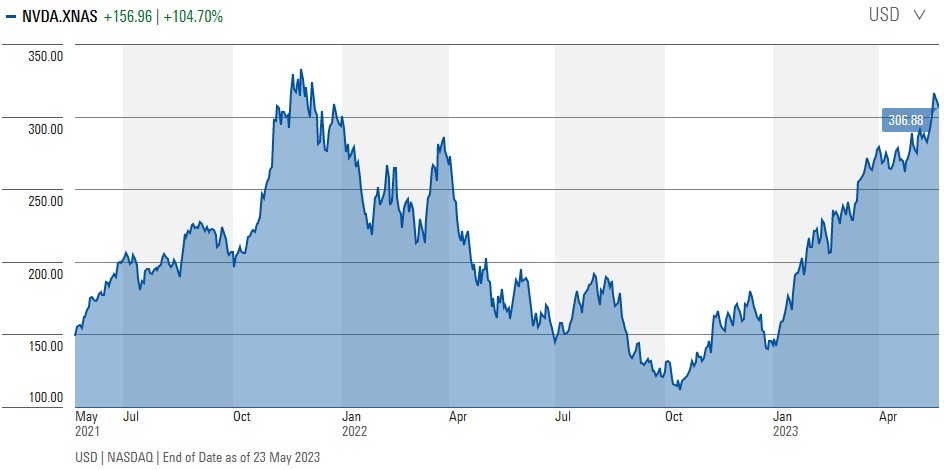

For example, emotions are running high in some investment teams as Nvidia's price rises and falls and rises with changing market sentiment towards AI. Despite its extraordinary rise in 2023, Nvidia is not back to the US$330 price reached in 2021. Pity the portfolio manager who bought in late 2021, giving up in October 2022 at US$112 as the stock collapsed, and it is now US$306. It's one thing to miss a trend like this. It's another to invest in it and exit just before it takes off again.

Source: Morningstar Premium

(Footnote to this comment on Nvidia, which was written on Wednesday 24 May, before Thursday's edition. The same day in the US, Nvidia released its quarterly results, and the future prospects so impressed the market that by the end of the week, the share price was up a further 30%, closing at US$389. Such massive short-term price movements for a major company, taking its P/E ratio above 200 and touching US$1 trillion in value, with a vast range of future estimates of its income, are rare in stockmarkets. We will cover this unusual event in more detail next week. This company has become the bellwether for the potential of AI).

I have sat in the same office as fund managers whose arguments with colleagues are so aggressive and vitriolic that it's a wonder they can work together. I have seen stockbrokers black-banned for months by fund managers who feel an order was filled badly or a piece of information was withheld. It can be a tense environment where losing 1% in returns can mean underperforming a benchmark. For large super funds, it might mean a warning must be issued to all fund members and ultimately the threat of closure.

At the 2023 Morningstar Investor Conference yesterday, Mark Delaney, the Chief Investment Officer at AustralianSuper, made the surprising statement that only one in three active managers comes good after a period of poor performance, and he had often been too slow to terminate a mandate.

“When you look back, you should have got rid of them when you first start to worry about them.”

And yet the index performance against which the manager is measured may be driven by market activity bordering on irrational, such as the BNPL or crypto or tech wreck frenzies. As Morgan Housel wrote on 'vicious traps':

"Years ago someone told me that bubbles happen when confidence (a good trait), optimism (a good trait), trust (generally good) mix to form greed and delusion. The reason bubbles are so common is that the inputs are mostly innocent, even if the output is lunacy and destruction."

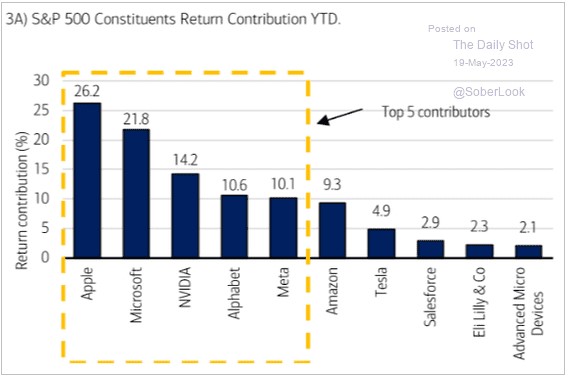

There is a remarkable event underway in the US which is driving up indexes (such as the S&P500 and NASDAQ) and causing massive winners and losers among global equity managers. When large companies make big moves, the funds which do not hold them are destined to deliver underperformance relative to their benchmark.

In calendar year 2023 to date, Apple, Microsoft, Nvidia, Alphabet and Meta account for over 80% of the S&P500's returns. This chart from The Daily Shot shows Apple and Microsoft alone have caused nearly half the rise in the S&P500, and any managed fund that does not own these two stocks will struggle to keep up.

Source: The Daily Shot

Source: The Daily Shot

We even see the strange position where fund reports explain performance in terms of stocks not held. Here is an example from an April report of a leading Australian global manager:

"POSITIVE CONTRIBUTORS

Tesla (no holding)

Tesla shares declined over 20% in April after reporting lacklustre Q1 2023 earnings. Tesla pushed through aggressive price cuts to fend off competitors which impacted margins. Despite the company’s manufacturing, brand, autonomous software, and US subsidies advantages, we believe the assumptions required to underwrite an acceptable return on Tesla shares are too high to justify holding a position in the Fund."

The fund did well in April because it did not hold Tesla. And many fund managers will soon report that they did poorly because they did not hold Nvidia and Microsoft.

Another side of the less-than-glamorous industry is when a fund simply cannot attract investors, and there are plenty that quietly shut down after starting with such optimism. We hear more about the successes but it's a grind if it doesn't work. For example, this week, Blue Orbit, a boutique small-cap fund manager formed in 2018 advised the market:

"After five years of hard work, real innovation, and a roller coaster ride of emotion, we are now selling/closing down Blue Orbit. The performance of our global small caps fund was very good - excellent versus most of our peers globally - but we were simply unable to raise enough funds. Both the global and Australian small caps funds are now closed."

It's tough. In the office by 7.00 each morning, read the newspapers, check every screen, meet with company management, slog through endless annual reports, debate furiously with colleagues, then do well but nobody wants you. Since inception, the fund was a decent 1.3% ahead of its index after fees when it last reported.

In funds management, it's difficult to know whether someone has a good track record because of skill, luck, membership of a talented team or because a particular style works for a while. While the data on active manager performance versus their benchmarks is not flattering, investors should be sympathetic if they miss out for while due to ignoring a bubble. Given time, they might be right.

***

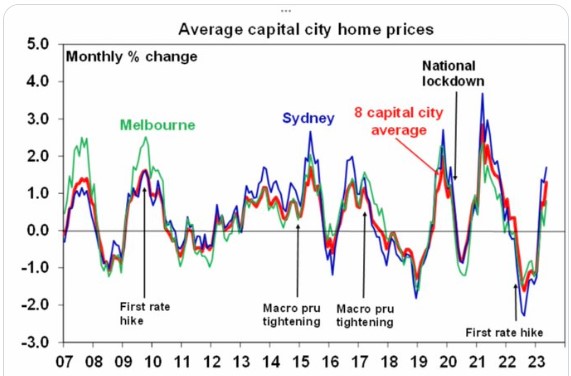

It is fascinating to watch residential property prices at the moment and speculate on the next year. As this chart from AMP's Shane Oliver shows, there is an unexpected price turnaround in the face of rising interest rates, due to high immigration, supply shortages and low availability of rental properties. Many people are helping their children to buy homes, and it may have implications for the cash rate. As Oliver says:

"Although the RBA does not target home prices, the rebound will be concerning them due to the reversal of the negative wealth effect, leading to a risk of more rate hikes."

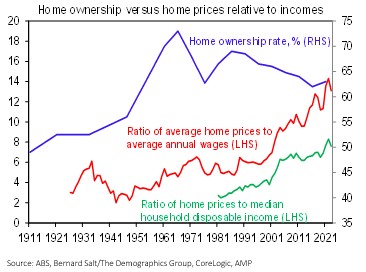

Drawing on work by Bernard Salt of The Demographics Group, Oliver looks at many factors to explain declining home ownership, from a peak of 73% in 1966. He says many younger people are now investing in other ways such as on the stock market, and spending more on personal experiences. But a leading cause must also be a decline in housing affordability, as shown in the red and green lines below.

***

The Twitterati enjoyed a fun but serious subject this week with many examples of the 'shrinkflation' of smaller product sizes sold at the same price as larger predecessors. The Reserve Bank focuses on all aspects of inflation and the implications for interest rates, and shrinkage deserves more attention.

Even without the shrinkflation, the UBS Evidence Lab tracked more than 60,000 prices in Coles and Woolworths and estimates that supermarket prices rose 9.6% in the 12 months to April 2023.

***

Many people approach retirement with a relatively simple plan: own their home, retain some investments outside super and leave as much as possible in super for its favourable tax treatment. Government policies encouraged this independence in retirement. The new tax on super balances over $3 million brings other options into play, and we check eight investment pools with different tax treatments.

Although there was supposed to be a consultation period on the new tax, Treasury officials have said both the $3 million threshold and the inclusion of unrealised gains as earnings are non-negotiable. Meg Heffron's monthly column also delves into the ways the new tax may make investing more complicated, with examples of anomalies Treasury is unlikely to have considered. As the start date of 30 June 2025 approaches, more complexity will surface.

Graham Hand

Also this week ...

Jack Gance is a rare entrepreneur who’s created two dominant market leaders from scratch, including Chemist Warehouse. In the article by Lawrence Lam of Lumenary Investment Management, Gance reveals how he did it: from finding business niches, to innovative marketing deals to scale a brand, and expanding business advantages through exclusive supplier deals, and treating suppliers well. It's a front row seat to the thinking of a great businessman.

It may be hard to believe, but Campbell Dawson of Elstree Investment Management reckons the competitive advantages of Australian banks are underappreciated. He thinks they're among the world's best banks because of their deposit-taking dominance. It makes bank hybrids a rock-solid investment, in his view.

Hugh Selby-Smith of Talaria Capital warns readers not to be sucked in by the recent market rally. He thinks we're at the risky end of the equity market cycle and it's time to play defence. That means investors should prize income, excellent value, short duration, and rapid payback periods.

ASX small companies have had a hard time recently, underperforming large companies by a considerable margin. Liquidity in these smaller stocks has also slowed to a trickle. Yet NovaPort Capital's Sinclair Currie says conditions are ripe for a turnaround, and he reveals which stocks have good upside.

Andrew Macken from Montaka Global Investments says investors needs to evolve and develop their skills. He outlines five steps to improve an investment toolkit, including thinking probabilistically, running your own race and measuring yourself objectively.

Two extra articles from Morningstar for the weekend. Morningstar has raised its fair value estimate for ChatGPT chip maker, Nvidia, by 50%, as Abhinav Davuluri reports, and Megan Neil suggests the recent fall in lithium stocks may be an opportunity for investors.

In this week's White Paper, ClearBridge Investments, part of Franklin Templeton, has tested the short- and long-term return profiles of infrastructure against a backdrop of changing macroeconomic factors.

***

Weekend market update

On Friday in the US, it was euphoric into the long weekend there, as the S&P 500 jumped another 1.4% to make fresh year-to-date highs while the Nasdaq ripped 2.6% to extend its 2023 gains to 31%. Treasurys flattened with the long bond settling at 3.95% from 4.01% the prior day and WTI rose to near US$73 a barrel while gold barely moved at US$1,947 per ounce. The VIX dropped below 18.

From AAP Netdesk:

In Australia, the local share market finished slightly higher on Friday amid reports US politicians were close to avoiding a catastrophic default, but the stand-off has still led to the worst week in two months for the bourse. The benchmark S&P/ASX200 index finished Friday up 16.6 points, or 0.23%, to 7,154.8, while the broader All Ordinaries closed up 18.2 points, or 0.25%, to 7,334.9. But after losses every other day this week, the ASX200 finished the week down 1.71%, its worst week since mid-March.

Tech was the ASX's best-performing sector on Friday, buoyed for a second day by enthusiasm over artificial intelligence after chipmaker Nvidia's rosy quarterly earnings report. Tech companies collectively gained 1.6% with printed circuitboard company Altium adding 3.6%, NextDC growing 3.5% and Appen climbing 1.2% as new-ish chief executive Armughan Ahmad used an artificial intelligence chatbot to welcome investors to the AI training company's annual general meeting in Sydney.

Fisher & Paykel Healthcare was the worst performer among the ASX200, falling 6.3% to a four-month low of $22.48 after the New Zealand respiratory products company announced a full-year profit of $NZ250m, down 34% from last year and $5m under expectations.

The heavyweight mining sector was up 0.9% after five straight days of losses amid concerns about China's recovery. BHP gained 1.4% to $42.75, Fortescue Metals added 3.3% to $19.62 and Rio Tinto climbed 2.3% to 107.77.

All of the Big Four banks finished higher, with NAB the best performer, adding 0.7% to $26.23. ANZ and CBA both gained 0.5%, to $23.47 and $98.16, respectively, while Westpac edged 0.1% higher to $20.92.

Latitude Financial Group fell 3.5% to a seven-week low of $1.25 after the personal finance company said it was unlikely to pay a half-year dividend and had set aside $46 million to pay for fallout from the massive hack of customer data from its systems in March.

Humm Group fell 8.2% to 39c after its buy now, pay later subsidiary received an interim stop order from the securities regulator temporarily forbidding it from signing up new customers.

From Shane Oliver, AMP:

Global share markets were mixed over the last week with uncertainty about the US debt ceiling and interest rates along with worries about the Chinese recovery, but a strong boost to some US tech stocks from strong AI related demand.

After a solid gain on Thursday and Friday, US shares rose 0.3% for the week. The Japanese share market continued its resurgence rising another 0.4%. However, for the week Eurozone shares fell 1.5% and Chinese shares fell 2.4%.

Bond yields rose globally and in Australia on increased expectations for rate hikes with the Australian money market pricing in just a 4% chance of a 0.25% RBA rate hike next month (which seems a bit too low) but a 72% chance by August. Oil prices rose, but metal and iron ore prices fell and the $A broke below technical support around $US0.66 as the $US rose further.

Apart from AI enthusiasm, the past week has been dominated by mixed news regarding the US debt ceiling where a deal seems to be coming together but there is a way to go yet with potential for further setbacks.

The message from central banks over the last week was mixed: the Bank of England looks certain to hike more given higher than expected UK inflation which may partly be due to Brexit; RBA Governor Lowe repeated his hawkish message to federal MPs warning of more hikes ahead in a reportedly “pretty pessimistic” briefing and warning that raising wages to match inflation without higher productivity would add to the problem – he’s right on wages as a key lesson of the 1970s is that wage rises to match inflation just perpetuated high inflation to the benefit of no one; the Fed looks unclear as to whether it will do more or not but does appear to be leaning to a pause next month although higher than expected personal consumption expenditure inflation in April increases the pressure for more rate hikes; the Bank of Korea and the central Bank of Indonesia left rates on hold; and the RBNZ after another hike signalled rates had likely peaked ahead of rate cuts in the September quarter next year.

Overall, our assessment remains that central banks are at or near the top on rates as inflation pressures are likely to continue to ease. This also applies to Australia where soft data, as seen in April retail sales, provides room for the RBA to leave rates on hold at its June meeting.

Curated by James Gruber and Leisa Bell

Latest updates

PDF version of Firstlinks Newsletter

Quarterly ETFInvestor (ETF Market Data) from Morningstar

ASX Listed Bond and Hybrid rate sheet from NAB/nabtrade

Listed Investment Company (LIC) Indicative NTA Report from Bell Potter

LIC Monthly Report from Morningstar

Plus updates and announcements on the Sponsor Noticeboard on our website