The cupboard is looking bare for the defensive allocation in a portfolio. The real cash rate in Australia is zero. The largest issuer of term deposits in Australia, the Commonwealth Bank, has a top rate out to 12 months of 3.55%, with many terms at 2.65% or less. There is no significant retail corporate bond market in Australia. The hybrids raising billions of dollars are higher risk and near the bottom of the capital structure. Bond funds are suffering price falls as longer term rates rise. High-yield equities are risky in a stock market propped up by money printing and low rates, and direct property is experiencing its own mini bubble and supply shortage – just join one of the queues at an off-the-plan launch in Sydney if you don’t believe it.

Where do term deposit investors turn as billions in the ‘safe cash’ allocation mature?

Investors who were enjoying term deposit rates of up to 6% in the last couple of years now realise that their biggest risk was not the credit on the bank (and deposits less than $250,000 carried a government guarantee anyway), it was the rollover risk of investing for short terms. Those who shied away from equities after near-death experiences in 2008 are now facing something that was never in their financial plan – effective returns after inflation of nil.

The biggest fear is that the risk-averse investor will go into equities or property out of desperation, facing a declining standard of living as 2.5% does not generate enough income. At some stage, they will be hit by a volatility of share prices which will cause sleepless nights.

So let’s look at the range of mainstream interest-earning assets available.

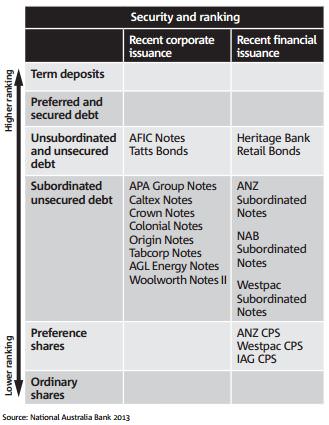

Priority of payment in event of liquidation

The most important starting point is where an investment sits in the risk spectrum.

Figure 1: Priority of payment in event of liquidation

Every investor must consider the consequences of moving away from the security of cash and term deposits held by banks, but the rate improvements are tempting. For example, at major banks:

- at-call cash account, 2.5%

- 12 month term deposit, 3.5%

- subordinated debt, for example recent Westpac issue priced at bank bill rate plus 2.3%, which currently totals about 4.8%

- hybrid (preference shares), based on recent ANZ issue, BBR plus 3.4%, or about 5.9%

- ordinary shares, adjusted for franking, say 7.5%.

The most appropriate alternative depends on each unique investor circumstance.

1. Online, direct at call offers

On the surface, the online savings accounts offered by many banks, including Rabobank, INGDirect, Ubank and ANZ Online, seem attractive, currently paying around 4.5%. But most have this special rate for the first 4 months only, which equates to 1.5% over that time (4.5%/3). For example, ING’s Savings Maximiser drops to a miserly 2.75%. It’s hardly worth the paperwork and effort for the short term ‘limited time only’ additional return, especially for an SMSF where several forms of identification are necessary to open a new account. Furthermore, the rate will drop in response to easing cash rates.

However, for the most risk averse, an online account which carries the government guarantee and which does not revert to a lower rate after 4 months is well worth considering, removing the argument with the bank each time a term deposit matures. For your 90-year-old mother-in-law, who may want access to cash, complete security and minimum paperwork, this is hard to beat.

2. Term deposits

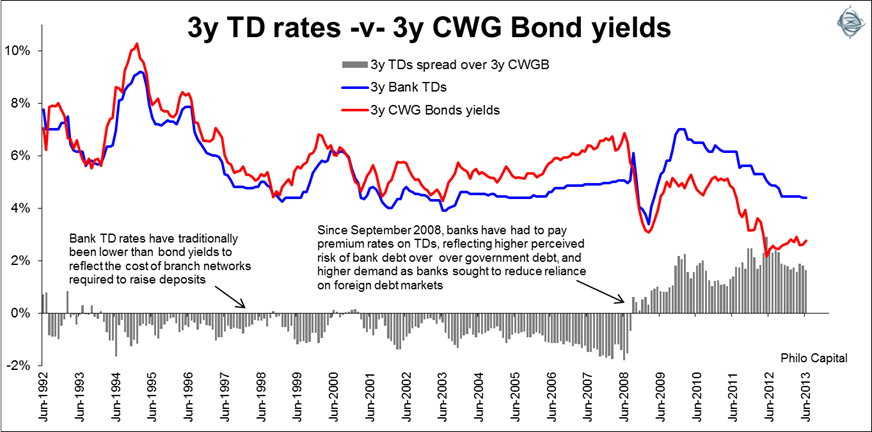

Prior to the GFC, banks issued few term deposits for longer than 12 months, and usually did not even match the government bond rates (CWG in the chart below). However, the GFC changed everything, not only as the banks competed hard for retail deposits to replace more volatile wholesale and offshore sources, but because investors sought the undoubted security of government bonds (in the pre guarantee days). Term deposits became the investment of choice for hundreds of billions of deposits fleeing the share market, desperate for a safe home, as rates rose well above government bonds.

While term deposits are the best quality investments generally available, the 3 to 4% returns are pushing investors away, even with ‘blackboard specials’. For undoubted security and a half-decent rate, there is a place in most portfolios for a term deposit allocation. By shopping around some of the international, less well-known banks in Australia, it’s possible to earn 4.5% for 3 to 5 years, with the comfort of the government guarantee. But this might be a stretch on the longevity side for the 90-year-old mother-in-law.

Another factor to watch is that wholesale bond markets now deliver a cheaper cost of funds than term deposits, and so banks will gradually wind back their term deposit rates. Even a smaller bank like Bendigo and Adelaide advised this week it was keeping deposit pricing “towards the bottom end of the competitive range” and leaning towards wholesale sources.

3. Subordinated debt and hybrids

Investors who normally go for term deposits have bought hybrid instruments by the billion, but most are sold to retail investors rather than institutional. This suggests they are not priced attractively enough. As the majority are issued by Australian banks, conservative retail investors have convinced themselves they are fine, in return for the yield pick up over the bank bill rate of between 2.3% (for the better subordinated) to 4% (for the lesser convertible preference shares).

This is not the place for a full review of the myriad structures offered in this space, where almost every transaction has its unique features, making like-for-like comparisons of margins almost impossible. To make a few points:

- APRA has tightened up the rules on capital eligibility, requiring bank convertible preference shares to have genuine loss-absorbing characteristics in stress conditions. In some issues, APRA can insist on a hybrid being converted to ordinary equity if it decides a bank would be non-viable without it, but APRA refuses to explain when this might occur. Arguably, some hybrids now carry the same risk as equity in an extreme event.

- Even before these strict clauses were introduced, hybrids gave investors little protection during the GFC. For example, as shown below, the Commonwealth Bank’s PERLS3 fell as low as $125 from its issue price of $200, a mark to market loss of 37%, and has not recovered pre GFC levels because spreads on bank capital instruments have repriced. The subsequent recovery is little comfort to those forced to sell in stress conditions.

Commonwealth Bank PERLS3 Prices 2006-2013

Source: CommSec

- In repayment rank, subordinated debt sits below term deposits but above the hybrid structures such as convertible preference shares, and conservative investors should probably limit themselves to this one rung down in the credit quality spectrum.

- The new hybrid structures are untested in stress conditions, which inevitably will face the banks again at some time. It is easy to be complacent about our best banks in stable times, but consider this recent quote from ASIC Commissioner, Greg Tanzer (AFR, 24 July 2013):

“The figures suggest, with respect to hybrids [interest-paying debt-equity instruments], the larger proportion are bought by retail investors, and a lesser proportion by institutional investors. That does give us some cause for concern about the extent to which people are appreciating the risks involved in that area.”

ASIC is further cracking down on hybrids, including this criticism:

“Spruiking the potential higher returns of hybrids and the brand name or reputation of the issuer without balancing that with the risks of the product can also cause investors to be misled.”

With the bank bill rate potentially heading to 2%, even with these hybrid spreads over 3%, investors will be earning only 5% or so for taking equity-like risks.

4. Bond and fixed interest pooled funds

Managed funds and ETFs help to diversify exposure by holding a wide range of securities, but they are marked to market each day, resulting in price fluctuations which many investors would rather avoid. Although cash rates have been falling, the 10 year Australian government bond yield has risen from a low of 2.9% on 3 October 2012, to about 3.7%. Bond prices are more volatile than most people realise – a 10 year bond yielding 2.5% will lose 19% of its value if rates rise to 5%, and 37% of value if rates rise to 8%. Such rises are unlikely but there is enough uncertainty in the world that it’s a tail risk worth thinking about, especially when the US enters its QE tapering.

The legendary fixed interest fund manager, Bill Gross of Pimco, controls US$268 billion in his flagship fixed interest fund, but it recently delivered a 4% loss in two months in the face of rising US Treasury rates. Gross compared the losses from his funds to one of the bloodiest battles in human history, the Battle of the Somme, where one million soldiers died, and his funds are in massive outflow. Even for long term investors, these are painful times for many bond fund holders.

While a direct holder of a term deposit or fixed rate bond may not actually mark their investment to market, knowing they will hold to maturity and be sure of a defined rate and a certain payment, all income-producing investments, whether they are marked-to-market or not, will behave like bonds and lose economic value when interest rates rise.

5. Unlisted corporate bonds

The lack of development of a quality corporate bond market which retail investors can access easily, supported by an active secondary market, is a major failing of the Australian financial system. There are nascent signs of its uprising, led by a few small brokers who specialise in fixed interest. These include FIIG Securities, Mason Stevens and Evans and Partners. The major investment banks such as UBS and Macquarie and their private wealth departments also source bonds for clients, but these services come at a significant cost, perhaps 1% or more of the balance under management. That’s quite a hit when rates are low.

A common requirement, however, to access these bonds is a Certificate under Section 708(8) of the Corporations Act, requiring the investor to be identified by a certified accountant as a sophisticated investor (net assets of at least $2.5 million or gross income of $250,000 a year). Once this hurdle is achieved, bonds can be bought in smaller parcels, usually with a $50,000 minimum but in FIIG’s case, a range of stocks is offered in $10,000 lots (but at a ‘retail’ price).

FIIG has probably done the most to deliver new corporate names to the market, introducing three heavily-oversubscribed borrowers in the last year – Silver Chef (8.5% for 6 years), Mackay Sugar (7.25% for 5 years) and G8 Education (7.65% for 6 years). All these bonds have rallied since issue. FIIG has also been at the forefront of offering inflation-linked bonds (for example, Sydney Airport 2020 and 2030 and Envestra 2025) while Mason Stevens has a speciality in attractive mortgage-backed security tranches (for example, a AA- tranche can be bought for about 325 basis points above 1 month bank bill rate).

These are all welcome developments, although obviously with higher returns come higher risks. These securities do not have the credit strength of bank term deposits, but they are well worth a look for qualifying investors. It’s a pity the top corporate names, such as Woolworths, Wesfarmers and BHP, are not supplying bonds to the retail market, to offer diversification away from the banks.

6. Listed corporate bonds

Take a look at the back of The Australian Financial Review and there is a section called ASX Interest Rate Securities. Under ‘Corporate Bonds’, it lists only the Heritage Bank transaction, as shown in Figure 1 above. Then there is a longer list of ‘Floating Rate Notes’, ‘Convertible Notes’ and ‘Hybrid Securities’.

While this is a pretty meagre list for a developed financial system like Australia’s, there are interesting opportunities worth exploring with a financial adviser. As they are listed on the ASX, they can be bought like ordinary shares in small volumes (but subject to brokerage costs), giving retail investors access to a wider variety than is often realised.

Simply to illustrate the point that there are listed corporate bonds out there, but not to recommend any of these in particular, here are a few examples:

- Peet Group is a residential real estate developer. In June 2011, it issued 500,000 convertible notes at $100 each with a fixed semi-annual coupon of 9.5% per annum. The maturity is 5 years, and it is cumulative and unsecured but ranks equally with all other unsubordinated debt. Ignoring the value of the conversion price, at its current market price of about 102.5%, it is yielding to maturity about 9%. Peet has a market capitalisation of $520 million.

- Whitefield is one of the longest established Listed Investment Companies in Australia, dating back to 1923. In August 2012, it issued $30 million (since increased to $40 million) of Convertible Resettable Preference shares paying a non-cumulative 7% fully franked dividend semi-annually, equivalent to 10% including franking. It matures in 2018, and the Net Tangible Assets are worth about $300 million supporting the preference shares of only $40 million. It is currently trading at about $115 to yield 6.7% to maturity.

- Heritage Bank Notes mature on 27 October 2014 and were issued with a 10% quarterly coupon, now trading at around 106.5% to yield around 6% to maturity. This is senior debt rather than subordinated or a hybrid, but issued by one of the smaller banks.

With any of these issues, there is a long Product Disclosure Statement, and the terms of repayment and obligations of the issuer are even more important than the interest rate. Repeating, these bonds are illustrative only of the way the ASX can provide some hidden fixed rate alternatives which are not exposed to further reductions in interest rates.

7. Annuities

At the moment, the majority of annuities sold are ‘term annuities’, issued for less than 10 years. They are term deposits by another name, usually backed by life companies rather than banks and commonly repaying part of the principal each year. For example, a $100,000 annuity for 6 years gives an annual ‘payment’ of $19,482 in the current market. This makes it difficult to compare rates on annuities with other products, which are quoted in rate terms, and investors must realise the principal is falling each year.

Annuities have grown strongly over recent years, aided by the commissions paid by life companies to advisers and the move to post-retirement planning. Lifetime annuities have also increased in popularity, and more recently, there has been innovation in the space, with both Westpac and National introducing ‘annuity deposits’. For example, Westpac’s has a minimum of $50,000 and terms out to 15 years. These fit into the term deposit category in terms of security.

8. Listed equities and property

Equities and property are included here for completeness, especially since investors are flooding out of term deposits into high-yielding stocks, listed real estate trusts and direct real estate. But these assets have completely different characteristics to cash and term deposits, are far more volatile, and place the investor in another world of risk.

What are some strategies to cope with the dilemma?

Most investors face a dilemma. They traditionally rolled over term deposit investments for 6 to 12 months, but must go out 3 to 7 years in search of yield and to bed down at least a minimum earning level. However, they are exposing themselves to rising rates which, even if not marked to market, leave the potential for underperformance. On the other hand, there is a convincing case that rates will stay lower for longer.

Here are a few strategies to manage both risks, assuming the investor is managing the portfolio rather than leaving it to a fund manager:

- stagger the term exposure into a series of 3 or 5 year investments, so that there is a regular maturity pattern

- limit the amount of a portfolio committed at fixed rates to the long term, say beyond 5 years, as nobody wants to live on 5% if rates rise to 8%

- shop around the international banks that are less well-known in Australia, that carry the government guarantee

- consider opportunities in high quality senior ranking corporate or infrastructure bonds for qualifying investors

- use a high yield at call account, but only where the rate does not fall away after 4 months

- don’t judge the quality of a hybrid by the name of the issuer – many of the new transactions have equity-like characteristics

- subordinated debt sits above preference shares in the capital structure, and may be as far down the credit table as many conservative retail investors should go.

And don’t load up on equities as an alternative to term deposits, but at the other extreme, don’t leave your money in a cash account earning negative real rates.

Disclaimer: the author owns many of the investment types described in this article, although he gains no financial advantage from the marketing and distribution of any of them.