In writing about debt and bond markets in the post-GFC sovereign debt crisis, I have often referred to Australia’s default. For example, I have compared it to recent defaults and debt restructures by countries like Greece in recent years. These references and comparisons have drawn much feedback from readers in Australia who have expressed surprise, shock and disbelief that Australia has defaulted on its government debts. This three-part series of articles tells the story of Australia’s big default.

Many countries, including the US and Australia, have defaulted on their debts at one time or another – i.e. they have failed to pay interest and/or principal on government bills, notes and bonds when due. In the case of the US, the three ‘defaults’ on US Treasury Bills by the US government in 1979 were temporary and quickly rectified. [See US Government shut-down – been there, done that, Cuffelinks, September 2013]

Australia’s 1931 default was a ‘big one’ – a full scale Greece-like permanent restructure of Australia’s entire stock of domestic debt owed to bond and note holders.

Domestic versus foreign debt

Governments of countries can borrow from their own citizens and/or they can borrow from foreigners if the pool of domestic savings of its citizens is not sufficient to fund their government deficits. Money borrowed by governments from their own citizens is generally payable in the local domestic currency.

On the other hand, governments of countries with relatively weak currencies or relatively unstable or immature political environments often need to raise debt denominated in a foreign, stronger, (or ‘sovereign’) currency – like the US dollar, pound Sterling or now the Euro - in order to attract foreign investors to lend them money. Foreign investors will often demand repayment in a ‘hard’ currency because the domestic currency can easily be devalued or debased by the government.

For example, would you lend your hard earned Australian dollars to Argentina’s government to be repaid in Argentine Pesos? Not likely. You would probably insist on repayment in a ‘hard’ currency like US dollars. (The Argentine Peso has fallen by 35% in the past year alone, so you would have lost 35% of your money had you lent your money in Pesos).

Government borrowing in a foreign ‘hard currency’ is usually termed ‘sovereign debt’ because borrowing in gold has been regarded as the ultimate ‘hard currency’ for loans for more than two thousand years. Even the mighty US of A had to resort to borrowing in foreign, harder currencies during its 1978-1979 government debt crisis. [See US Government has previously defaulted, it’s not risk-free, Cuffelinks, October 2013]

Defaulting on government debt

Governments usually don’t default outright on, or restructure, their domestic debt (debt issued in their own currency and owned by their own citizens) because they generally don’t need to. If the Australian government suddenly decided to pay only 97 cents in the dollar on the money it owed on interest and principal obligations that were due for payment in 2015, then 94 cents in the dollar on money due in 2016, and 91 cents on money due in 2017, and so on, there would be riots in the streets and the government would probably be thrown out for reneging on its obligations to repay money it owed when due.

A more subtle and surreptitious way of achieving a similar outcome (ie repaying less than the government owes) is for the government to create domestic inflation and/or unilaterally declare a new arbitrary value of its paper money and then repay the debts with the new devalued paper. This practice has also been going on for more than two thousand years. One of the earliest recorded examples of this was by Dionysius, ruler of Syracuse (405 – 367 BC) in Sicily during the wars between the Corinthians, Athenians and Carthaginians for control of Syracuse. [See Catapults and coin tricks: what Ben Bernanke learned from the Greeks, Cuffelinks, January 2013]

Creating inflation to avoid paying full value

Governments have been creating inflation and printing money to pay off their debts with debased currency of lower real value ever since then, and they continue to do so today. Creating inflation by printing paper money is currently the flavour of the month with the major central banks of the world, with the US Federal Reserve, Bank of England, Swiss National Bank and the Bank of Japan leading the global charge.

All governments deliberately set out, as a matter of formal government policy, to create inflation to deliberately destroy the value of their own currencies, so that money they are legally obliged to pay in the future has less value than it does today. (Inflation has other side-effects that are seen by governments as being positive: it assists exporters, and it also creates an incentive for consumers to spend money rather than save it, as spending is seen perversely as more productive than saving, at least in the short term).

Australia leads the pack

Australia’s formal inflation target of 2% to 3% per year is the highest official inflation target in the world. It is a formal government policy to deliberately destroy the value of the wealth held by its own citizens by 2% to 3% each year!

This is why Australia has a fundamentally weak currency (relative to ‘hard’ currencies), and it is why Australia has the highest inflation rate and the highest interest rates in the developed world.

Japan – no way out but inflation

Japan has the biggest pile of government debt in the world (relative to its national output). Creating inflation to destroy the real value of the yen is the only way out of its current debt situation. There is no other way of paying it off – with Japan’s declining population, declining workforce, declining tax-payer base, and increasing welfare burden as its population ages rapidly. 95% of Japan’s government debt is owed to its own citizens so it can just print more yen to pay it off. The main stated goal of the ‘Abenomics’ policies in Japan is to create inflation – i.e. to destroy the real value of the yen – in order to assist exporters, to encourage spending, and to repay debts in debased yen.

Australia’s debt pile leading up to the default

Australia has always been a country with a relatively young population with a relatively small savings base of its own, and so it has always had to rely on ‘imported savings’ in the form of foreign debt and foreign equity for capital to fund its development.

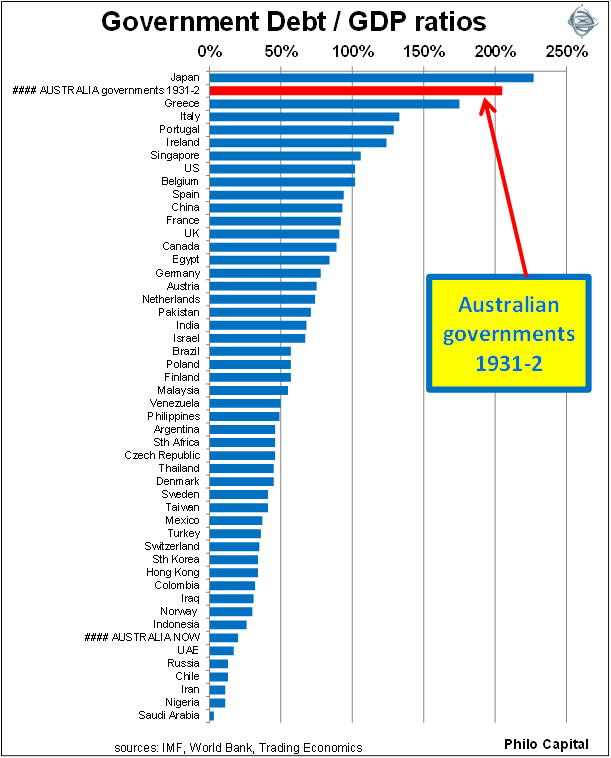

By 1932 Australia’s government debt to GDP ratio reached 205% - on par with Japan today. However, unlike Japan, 55% of Australia’s government debt was foreign debt. This was borrowed mainly from UK banks, repayable in London in Pounds Sterling, and traded on the London Stock Exchange. The rest was borrowed from Australian citizens and Australian institutions like insurance companies, and traded on the local stock exchanges – mainly Melbourne and Sydney.

Only 30% of the total government debt was Commonwealth government debt. The Commonwealth government only started to borrow money in a big way in the First World War but, under pressure from London bankers who had turned off the taps to the States in 1929, the Commonwealth government assumed responsibility for State debts. NSW was the most profligate state and had a disproportionately large share of debt, mostly to fund infrastructure projects like the rail and road networks.

The following chart shows Australia’s government debt level in 1931-1932 as a per cent of national output (GDP) compared with the debt ratios of the top 50 countries today.

We can see from this chart that Australia’s government debt at the height of the 1930s crisis was worse than any other country today except Japan, and much worse than Greece, Ireland, Argentina and Venezuela. In contrast, Australia’s government debt levels today are near the bottom of the chart.

Crippling interest burden

The interest burden on total government debts consumed a massive 40% of all government revenues in the 1920s and 1930s (compared to just 4% today). The problem was that total tax revenues were only 16% of GDP (23% today), and this left a massive hole in government finances. With Australia excluded from foreign debt markets from 1929 onward, and the pool of domestic savings hit by the depression, there was no other way out of the crisis but to default on interest payments and maturing principal repayments. The commercial banks and the Commonwealth Bank, which was the government's wholly owned banker and central bank, all refused to lend it more money. Something had to give.

In Part 2 of this story we look at how this happened, which bond holders were rescued, and which were forced to take a ‘haircut’ on their interest and principal repayments.

Ashley Owen is Joint CEO of Philo Capital Advisers and a director and adviser to the Third Link Growth Fund.