There are many changes happening in the macro-economic world. Here are the key points that will impact investment portfolios this year and beyond.

No going back to pre-Covid times

The world continues to adjust to the macro-economic and geo-political shift that has occurred since Covid. For 30 years interest rates fell with asset prices responding to cheap money and increasing in value. This correction is well underway as increasing interest rates are causing asset prices to fall and are reducing demand. Interest rates will soon reach a point of 'equilibrium', i.e., terminal value high enough to bring the Consumer Price Index (CPI) down.

US M2 (money supply) best demonstrates this new paradigm, having fallen recently for the first time since 1960. A reduction in money supply means that the US Federal Reserve via banks is withdrawing US dollars from the global financial system in its fight against inflation while at the same time there is an increase in demand for US dollars (see below Triffen’s dilemma), as international borrowers of US dollars require more US dollars to meet their increasing debt servicing costs.

To his credit, the Chairman of the US Federal Reserve, Jerome Powell, is doing what he said he would do. He is increasing the Fed Funds Rate to kill off inflation even if the main yield curves are inverted which indicate that rates should fall, and this is why the market is talking of the Fed pivot and is now rallying. Inflation hurts everyone while unemployment impacts few.

Australia is well placed

The positives for Australia are that unemployment remains low and folks have been spending during the Christmas and New Year holiday period. Yet this will slow down as the increases in interest rates flow through to mortgage rates and reduce household disposable incomes. Consumers will re-assess their budgets after the school holidays and find they need to reduce their discretionary spending, e.g., eat out once per week rather than three times, or cancel their Netflix subscription, etc.

Even with higher interest rates Australia is well placed to ride through the global slow down because it has a surplus of energy (food and resources), many mortgage holders are in front on their loans or they fixed their rate in 2021 when rates were low. Importantly, Australia’s Debt to Gross Domestic Product (GDP) ratio is low unlike the US, Japan and the Eurozone which are all well over 100%.

Federal Reserve Put

The 'Fed Put' is the financial market belief that the US Federal Reserve will step in to rescue the markets if equity prices fall too much. Over the last 20 years this can be seen by comparing S&P 500 index which moved in lock step with increases and decreases in the US Fed’s balance sheet. Powell wants to end this belief, even though he has not explicitly stated this as a goal. The Fed does not want to be captive of the financial markets, nor should it be.

US economy

Some key points:

1. Unlike in Australia, US fiscal policy is not aligned with US monetary policy. The US Fed is increasing interest rates while Congress continues to pass major stimulus packages, the most recent being US$1.7 trillion.

2. The US Fed (and all central banks) can only influence the short end (i.e., cash and bill rates) of the yield curve, whereas the 2-year to 30-year interest rates are determined by the market.

3. The US Fed will put the needs of the US domestic economy first (see Triffen’s dilemma below) over the needs of the international community.

4. US has been in a mild recession for 9 months (as a real GDP growth has been negative for three quarters) and key indicators such as the Purchasing Managers Index (PMI) and CPI are now falling, as well as key interest rate yield curves, e.g., US 10-year treasury, remain inverted.

5. The US is a debtor nation compared to 30 years ago when it was a creditor nation. It has the so called 'twin deficits'. There is a budget deficit of around US$3.5 trillion per year and a current account deficit. National debt of US$33 trillion, plus unfunded liabilities for defined benefit pension funds, student loans, etc. The US economy would be much worse if the US dollar wasn't the world's reserve currency.

6. The US debt ceiling has been reached again. We expect an increase as this has been treated historically by both Democrats and Republicans as a political event rather than as checkpoint to take action to address the structural problems with the US budget.

7. US savings rate is 2.5%, as most Americans live pay cheque to pay cheque. Whereas China’s saving rate is about 45% which is the highest globally except for Singapore. This high savings rate provides China with the capital to invest, including buying US treasuries to fund US debt.

8. US credit card interest rates on average are now 19.6% which is very high when considered in the context of many Americans living pay cheque to pay cheque.

9. US technology companies in 2022 have been downsizing having laid off 70,000 employees. Amazon (18,000), Alphabet (12,000) Microsoft (10,000) and Salesforce (7,000) and more likely to come in 2023, particularly in the crypto currency space. It is reported that Twitter has laid off 6,000 staff, or 80% of its full-time staff.

Triffen’s dilemma: world reserve currency v domestic economic requirements

The US Fed is facing Triffen’s dilemma. This happens only where an individual country's currency is used as the world’s reserve currency, as is the case with USD. There comes a point when there is a conflict between the world’s needs of the reserve currency with the needs of the domestic economy of that currency. When this situation arises, domestic politics and needs of the domestic economy trump those of the world.

We are currently seeing Triffen’s dilemma played out as the US Fed is restricting money supply through higher US interest rates, whereas the rest of the world needs more US dollars because the higher interest rates are increasing their debt servicing costs. In 2022, the US dollar appreciated significantly against all major currencies, although in the last few months of 2022 it fell back some.

Source: Trading Economics

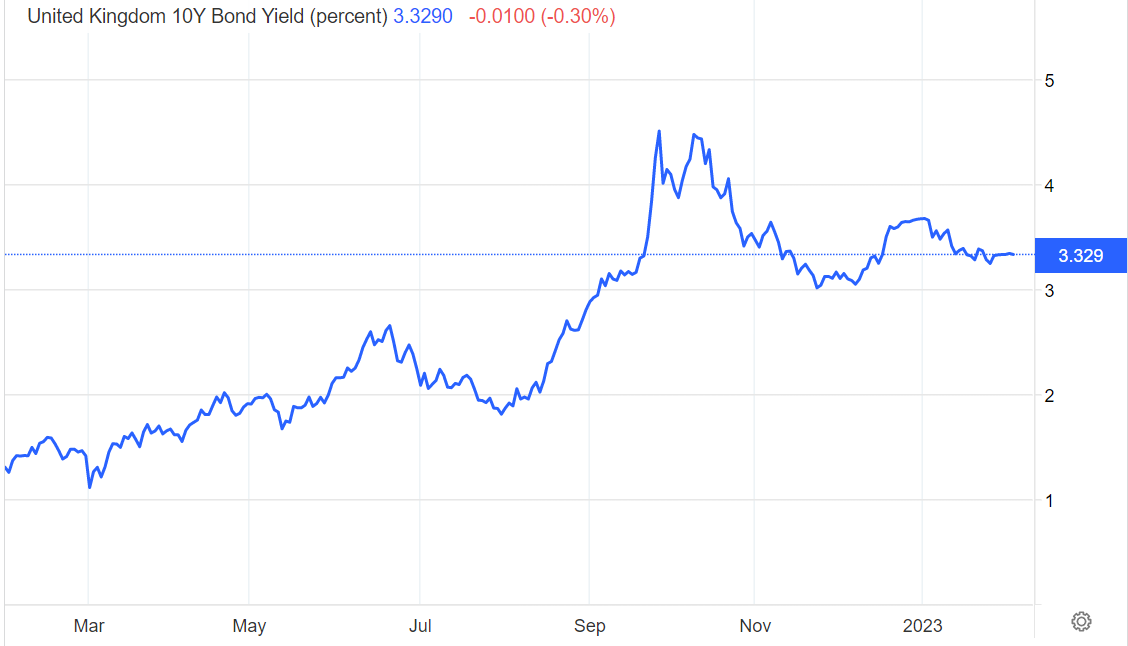

Currency versus government bond market

When forced to choose between supporting their currency or supporting the bond market, central banks always choose the bond market. If the government bond market collapses, a government cannot raise any more money and it can lead to a banking crisis. The UK recently witnessed this scenario as the Bank of England was forced to step in to support the gilt (bond) market and prevent its collapse, while allowing the UK Pound to devalue.

The world normally associates a currency and bond market crisis with third world economies, but not first world countries like the UK.

Source: Trading Economics

De-dollarisation

Sanctions imposed on Russia because of the invasion of Ukraine include the US and its allies freezing US$300 billion of Russia’s reserves. For many years US governments have weaponised the US dollar. This has led to autocratic countries such as China and Russia increasing their pace of de-dollarisation -quickly moving to transact in their local currencies, i.e., non-US dollars and possibly tied to gold in some manner.

Countries that have historically aligned themselves with the US, such as Brazil, India, and Saudi Arabia, are taking preliminary steps to be part of this movement as they do not wish to find themselves sanctioned and their foreign reserves frozen because the US does not 'approve' of an action they may have taken.

This does not mean the imminent end of the US dollar as the world reserve currency as there is no obvious replacement. Rather, there will be less reliance on it in bi-lateral trade between countries outside the US. A good example is that Argentina and Brazil are exploring having a single currency, so bi-lateral trade will not have to be transacted (converted) through US dollars. Such a step does not come without risk as those countries that joined the Euro can attest.

Energy is life

The energy market continues to see shortages because of the Ukraine war and an increase in demand because of the end of Covid lock downs. These energy shortages have caused major price increases and disruptions to businesses in several countries, where governments have been forced to take fast and extreme action. For example, over the 6 months to December 2022, the German Government spent US$500 billion on bringing old coal burning fire generators back online and in buying coal, gas and oil, as well as compensating businesses and consumers for the higher energy costs via subsidies and rebates. The German Government must be congratulated on the speed taken to address the shortage problem; however, it does reveal Germany’s reliance on fossil fuels.

End of the traditional 60/40 balanced investment portfolio

Another example of the world not going back to pre-Covid days is the traditional balanced investment portfolio model of 60/40 equities/bonds failed to provide positive returns where normally they compensate each other. In 2022, both bond and equity prices fell for the first time in 30 years with the S&P 500 index down by 19.2% and the US bond market (long-term US Treasuries) down by 29.3%. This investment model may not work in the new macro-economic paradigm.

The world is not going back to pre-Covid and pre-Ukraine war days and investors must come to grips with many changes.

Michael McAlary is CEO and Managing Director of strategic risk consulting firm Chairmont Group. This article is general information and does not consider the circumstances of any investor.