The Weekend Edition includes a market update (after the editorial) plus Morningstar adds links to two highlights from the week.

All investors use a logic and an intuition to guide which investments are most suitable, and investors develop and modify decision-making as their knowledge grows. Along the way, they meet people with different views, sometimes so confidently and expertly expressed that they may influence a change in beliefs. Investing is as much art as science and there are few absolutes, especially in the market conditions we currently face.

In my 45-year career, I have attended thousands of meetings, including with both the smartest and the most inept characters ever to carry a business card. When I was responsible for global funding at Commonwealth Bank and State Bank of NSW, we hosted domestic and overseas bankers every day, and each visitor came with a banter, an opinion and something to sell. The vast majority of encounters are buried in the back of what's left of my hippocampus, never to be retrieved.

But some meetings stay prominently in the memory, and one in about 1990 or 1991 included a lesson I will never forget. Short-term interest rates were around 16% to 18%, as shown below, and five-year rates were heading down from 15%. It was the time of the "recession we had to have" and inflation was rife and an accepted part of the investment landscape. Nobody thought 'normal' for interest rates would ever approach 2% or 3%.

Reserve Bank of Australia Cash Rates 1990 to 2022

At this time, the leading house in Australian fixed interest and bonds was Dominguez Barry Samuel Montagu, or DBSM. In May 1991, a majority stake was acquired by Swiss Bank Corporation which made its position even stronger. One day, a senior executive from DBSM presented to us an idea for a major transaction, which went something like:

"We've seen the five-year swap rate at 15% and it's heading down, but in my experience, whenever it hits 12%, it always bounces up off this level. We should arrange a major fixed rate issue for you at 12% and you leave it fixed, ready to lend at higher rates after the bounce."

Our risk management processes were sophisticated and we did not appreciate an investment banker telling us how to take advantage of rising rates as a way of generating a bond placement fee. But what stuck in my mind was his confidence based on his vast experience. He was absolutely sure rates would bounce off 12%. We ignored his advice and never did the transaction, and the deal would have been very expensive, as rates fell well beyond his magic 12% barrier.

And so to today. Prior to the last six months, it was commonly accepted that inflation and interest rates were very low and built into the economic system. Central banks were struggling to push inflation into a preferred 2% to 3% band. Tech innovation and improving global logistics were driving down prices. Then in FY22, for the first time in 30 years, in the face of a central bank switch to control inflation, all asset categories in a diversified fund (except cash) fell significantly in price.

For a range of reasons - the Ukrainian war, the Chinese threat, declining global trade, food and energy inflation, demographic challenges - it feels like a reset of our expectations.

Former Leader of the Opposition, noted economist and university professor, John Hewson wrote in The Saturday Paper:

"I have been analysing and forecasting economies since joining the International Monetary Fund in the late 1960s, and I can say it is much more difficult now than at any time since then to predict how the world and our economy will evolve. Multiple global liquidity injections, stretching back to the Alan Greenspan era of the early 2000s through to the responses to the 2008 global financial crisis, and most recently to the pandemic, have finally released the inflation genie. As a result, major central banks are reversing their easy monetary policy settings and rapidly raising interest rates." (my bolding)

Investors need to consider if we are in a new paradigm. What if interest rates rise to 5% or more? Are the days of inflation below 2% over? Has global population peaked, with implications for economic growth? Do the tools we use to manage the economy work as we expect? As US author and geopolitical analyst Peter Zeihan says in his most recent video:

"The relationships between all of the tools that we use to regulate the economy might not apply anymore. For the bulk of modern human history, the last 500 years, it's all about figuring out how you can maximise your share of a pie that is steadily growing. We've had steadily growing population growth turning into explosive population growth in the industrial era that postdates World War Two. And as long as there are more people, as long as there is more technology, growth is easy. And regulating inflation and growth and employment all the rest of that environment is something we have a lot of experience in. But that's not the case anymore. The global population is in the process of peaking. The advanced world population has long since peaked ... if the pie is no longer getting bigger, then it's not clear that any of our measures, whether it's for inflation, or growth or investment, or otherwise, are even relevant anymore, much less tools like interest rates ... They (policymakers) are literally making this up as we go along." (my bolding).

The Reserve Bank is making its decisions month-by-month "guided by the incoming data" having learned the lesson not to predict years ahead. The different views of the major bank economists shows how difficult predicting the next step has become. While Westpac and ANZ see the cash rate peaking at 3.35% this year, CBA and NAB are at 2.5%. That's a difference of more than three 0.25% increases in the space of a few months, and 3.35% is a long way from the current 1.85%.

Another lesson from the 1980s and 1990s is that central banks struggled to control inflation and went hard on rates to reduce demand. The Reserve Bank may overreact on the upside in the same way it overreacted on the downside for too long in 2021.

Regardless of what we think will happen, we should not to be as dogmatic as my friend in 1990. Rates bounce off 12%, right? Companies are coping with profound changes and there is a strong case that returns will be subdued for a while. Global geopolitical problems are not going away soon.

Complicating the investment decision is that stockmarkets often recover when economic conditions are at their worst. Even if interest rates and economic growth are known with 100% certainty, the market reaction remains a mystery. The NASDAQ is now up 20% from its June 2022 lows, despite the same recession and inflation threats that pushed it down over the previous six months.

In this context, the article by Julian McCormack is timely as he discusses the paradox of investing. When investors are lulled into confidence and certainty, as in 2021 coming out of the pandemic, that's when a new cycle kicks in:

"It is investors’ certainty that they are in unprecedented times, armed with better information than ever and standing on the cusp of hitherto unseen technological wonders, which leads them into the paradox of cycles. It is only when investors are certain they are not in a cycle, that truly wild cycles can emerge."

The Reserve Bank wants to talk down inflation and economic activity while engineering a soft landing, and although only one-third of Australians have a mortgage, the threat of falling house prices and rising mortgage repayments is already playing into consumer confidence. As Alex Joiner, the IFM Economist says:

"When weighing up the business and consumer sentiment outcomes today, it's notable that households account for around 53% of the real economy via spending. So while business sentiment likely means people keep their jobs, if they also stop spending, growth will unravel."

What about in the US? On Wednesday night our time, the year-on-year CPI was down to 8.5% from 9.1%, as shown below. The market jumped on the optimism that inflation may have peaked, with falls of 8% in petrol and a 11% in household gas prices (shaded areas are recessions).

US CPI, 12-month percentage change, all items

Source: US Bureau of Labor Statistics

Source: US Bureau of Labor Statistics

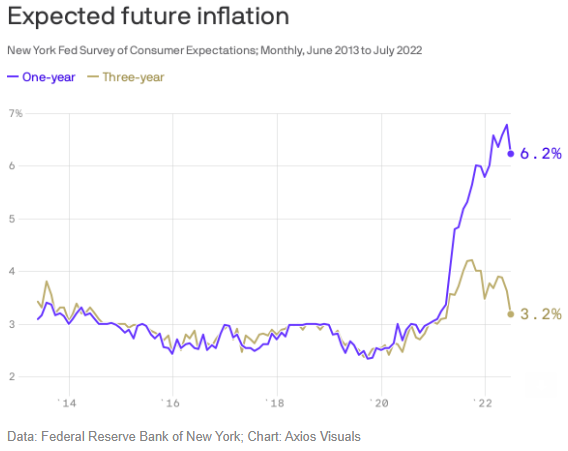

In addition, respondents to the Federal Reserve Bank of New York survey in July expect inflation to grow at a 6.2% pace over the next year, down from 6.8% in June, while the three-year number is 3.2%, down from 3.6% predicted in June. The main driver is the easing of fuel prices and food categories. According to David Kelly, Chief Global Strategist at JPMorgan:

"Overall, with demand slowing and supply picking up, we expect to see steady downward pressure on inflation for the rest of this year and in 2023 even if the Federal Reserve pursues a slightly less hawkish path."

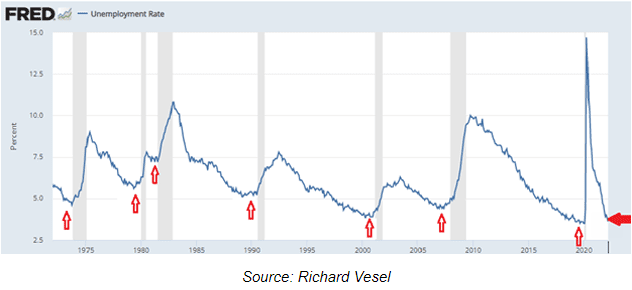

Meanwhile, John Mauldin, another US commentator, included a revealing chart in his newsletter this week. The shaded areas are US recessions, mapped against the US unemployment rate. It suggests unemployment bottoms just before a recession, as jobs growth comes from an overheated economy which drives up inflation.

In this week's edition ...

While we don't usually focus on company earning results, this current August Reporting Season is shaping up as one of the more important. Reece Birtles says it will show which companies and sectors are managing to control costs and pass on price increases, and there are likely to be extremes, as US results have showed recently. Then Rudi Filapek-Vandyck looks at some results which have already issued for resources, property trusts and asset managers for early signs that there will be winners among the strugglers.

Remember when Macquarie Bank and its various complex structures were the successful bidders for Sydney Airport back in 2002? It was all over the news, and even Alan Jones on Radio 2GB laughed at the ridiculous $5.6 billion paid, way more than the underbidders. Of course, Macquarie had the last laugh as they forced us to walk through duty free to reach the departure gates, raised parking fees because we had nowhere else to go, and built hotels and retail space. Stuart Cartledge was an investor for 20 years until the March 2022 sale for $32 billion, and it's fascinating to read an insider view in a case study transaction.

Ethical and sustainable and ESG funds have faced challenges in calendar 2022 as global oil and commodity shortages led to a surge in energy and resource companies often not held in these types of funds. Angus Dennis explains how the managers have approached this period, he shows how his ethical fund differs from the index, and why the fund's stance pays off over time.

Then Brian Feroldi, a US author and investor, gives a snapshot of 10 common mistakes that new investors make. Perhaps everyone should go through a stage of learning these lessons while there's not much capital at risk. Feroldi admits he made each of the mistakes in his early days, and he gives US stock examples.

To many investors, RMBS, or Residential Mortgage Backed Securities, may seem arcane, but they are issued by the billion each year in Australia to finance housing loans. While wholesale investors may be able to access directly from a broker, retail can invest via a managed fund, ETF or Listed Investment Company. Ashley Burtenshaw explains how they work and why no Australian investor has lost money on a domestic RMBS to date.

Two stock highlights this week from Morningstar. Christine St Anne discusses with analysts the profit results of QBE, Suncorp and CBA, while Nicola Chand reports on OZ Minerals rejecting the billion-dollar takeover offer by BHP and expectations of a higher bid.

This week's White Paper from Epoch Investment Partners, affiliated in Australia with our sponsor, GSFM, asks a somewhat satirical question about selfish companies denying consumers cheap products. But earning good returns on capital is not an obstacle to satisfying consumer demands. It is what enables companies to continue to invest to meet those demands.

A footnote to our article last week arguing the Reserve Bank's reliance on quarterly CPI data was unacceptable. The Australian Bureau of Statistics announced that from 1 October 2022, it will provide monthly CPI data, accepting that policy settings need more up-to-date information.

***

Weekend market update

On Friday in the US, the stockmarket was strong with the S&P500 up 1.7% and now recovering half of the fall delivered since to start of 2002 until mid-June. The NASDAQ rose 2.1%, continuing the tech optimism.

From AAP Netdesk: The local bourse has given up some of this week's gains despite strength from the energy sector but still managed to finish in the green for a fourth week in a row. The benchmark S&P/ASX200 index on Friday finished down 38 points, or 0.5% to 7,033. The energy sector was up 2.3% for its best day in nearly three weeks after the International Energy Agency raised demand forecasts. Woodside gained 3.7% and Whitehaven Coal finished up 2.5% to an all-time closing high of $6.62.

There was plenty of company-specific news as more Australian companies reported their full-year earnings results. IAG was up 1.1% to $4.66 after beating consensus estimates, although the insurance giant also cut its dividend after an extraordinary year for natural perils claims. Woolworths gained 0.1% to $38.05 after the Australian Competition & Consumer Commission decided not to oppose its $243 million acquisition of MyDeal.com.au. Three of the four big banks finished higher, with ANZ up 0.5% and Westpac and NAB both up 0.8%. CBA, which reported on Wednesday, dropped 0.5% to $100.34, its fourth straight day of declines. The heavyweight mining sector was down 0.7%.

From Shane Oliver, AMP:

The share market rebound continued over the last week helped by weaker than expected US inflation data. For the week US shares rose 3.3%, Eurozone shares gained 1.5%, Japanese shares rose 1.3% and Chinese shares rose 0.8%. Australian shares only rose 0.2% with strong gains in resources largely offset by sharp falls in IT, health and property shares. Bond yields generally rose as the fall in yields in prior weeks had gone a little too far too fast. Oil prices rose partly due to US supply disruptions and increased demand forecasts. Metal and iron ore prices also rose. The $A rose as the $US fell.

More signs of 'peak inflation' in the US. CPI inflation came in weaker than expected in July at 8.5%yoy (down from 9.1%) with core inflation remaining unchanged at 5.9%yoy and down from a peak of 6.5% in March. The decline in inflation came from lower gasoline prices (which has continued) and softness in prices for used vehicle, airfares and hotels. Producer and import prices also fell with annual inflation in both continuing to trend down further adding to evidence of peak US inflation.

Its premature to get too excited just yet. US goods price inflation has slowed and is likely to fall further - reflecting rising inventories, lower delivery times and falling freight rates - and energy inflation may also have peaked depending on the oil price. However, services inflation is still trending up reflecting rising labour costs (which are more sticky) and this is reflected in a still rising breadth of price rises with the median inflation rate rising to a new high of 6.3%yoy and the proportion of CPI components with price gains above 3%yoy rising to 89%. And of course, it will take a while to get inflation back to target. So more rate hikes from the Fed still lie ahead.

Graham Hand

A full PDF version of this week’s newsletter articles will be loaded into this editorial on our website by midday.

Latest updates

PDF version of Firstlinks Newsletter

VanEck webinar - 5 ideas for the inflation era, Tuesday 23 August 2022, 11:00am AEST.

Monthly Investment Products update from ASX

ETF Quarterly Report from Vanguard

ASX Listed Bond and Hybrid rate sheet from NAB/nabtrade

Indicative Listed Investment Company (LIC) NTA Report from Bell Potter

LIC (LMI) Monthly Review from Independent Investment Research

Plus updates and announcements on the Sponsor Noticeboard on our website