The Weekend Edition includes a market update (after the editorial) plus Morningstar adds links to two additional articles.

It's often the case that the greatest strength of someone is also their biggest weakness. Many of the world's most popular entertainers - Elvis Presley, Freddy Mercury, Michael Jackson, Jimi Hendrix, Janis Joplin, etc - died young as they struggled to cope with the fame and fortune that came from their prodigious talents. The personality attributes that thrived on the adoration of a global stage came with a predisposition to unhealthy behaviour. There's even an academic study called 'Dying to be famous' which concludes:

"Adverse experiences in early life may leave some predisposed to health-damaging behaviours, with fame and extreme wealth providing greater opportunities to engage in risk-taking."

Similar positives and negatives are evident in business and politics. Leaders with the self-confidence and conviction to run their countries are often belligerent, power-hungry and myopic, and there is no shortage of recent examples in Australia, the UK, Russia, the US and Italy. Many senior executives are difficult to work with and reach the top with a hard-nosed attitude to stakeholders (including their own staff) other than shareholders, who love them. Successful sportsmen and women are often so focussed on their craft that they have little time and space for anything else.

There's also a body of psychological work which suggests that extremes of 'desirable' personality traits might make it difficult to adapt to new or difficult circumstances. Think sports stars in retirement, for example. There is:

"an emerging perspective on why and how extreme standing on 'desirable' trait continua translates into maladaptive behavior and undesirable outcomes at work and in life."

There is evidence of the same extreme attributes in many aspects of financial markets, such as fund managers who fail to adapt to changes in opportunities and expect the old paradigms to continue. They fall in love with stocks and market assumptions and overlook threats, and miss the signs until it is too late. Experts who were media heroes with special insights into the future until their luck changes and their strut turns to shock.

It's the same with the workings of stockmarkets. The best features of an exchange are the ability to buy and sell instantly and cheaply in an open market at public prices. These are also the worst features. Easy liquidity facilitates attempts to time the market, increases turnover, incurs transaction costs and encourages responses to short-term noise.

It would be better for most people to establish a quality equity portfolio and not touch it for 20 or 30 years, until needed to live on. As Warren Buffett said:

"Only buy something that you'd be perfectly happy to hold if the market shut down for 10 years."

Daily liquidity is a drawback for investors who are unable to control the urge to buy when markets are running high and sell when in the doldrums. There is too much focus on the market's fluctuations and not the company itself, which may continue to run a strong business and pay increasing dividends regardless of its share price.

Home ownership thrives on better behaviour. Most older Australians have built their wealth by buying their own home rather than the perceived riskier method of owning shares. Not only does home equity allow a leveraged exposure to a (usually) rising market, but the owner permits the investment to compound over long periods, often decades. We lived in our previous home for 32 years. The same amount of money placed in equity markets would do at least as well but the price fluctuations are too much to bear.

I think back to an investment property I bought in 1993 for $300,000. I was tempted to sell a couple of times when the economic outlook was poor and I contacted real estate agents. They were not confident of a decent price during, say, the GFC, and so I hung onto it. If I had been able to reduce my exposure, by selling a bathroom or a bedroom in a liquid market, I would certainly have sold. Hanging onto the place for 30 years now gives me a property worth about $2 million which I would not have achieved in shares.

In case that sounds like a great return, turning $300,000 into $2 million over 30 years requires an annual compounding of only 6.5%, although the property has delivered an additional 3% or so in annual rents after costs. As the article shows in the Morningstar Asset Class Gameboard, the average annual return over the last 20 years in Australian equities is 10.2%.

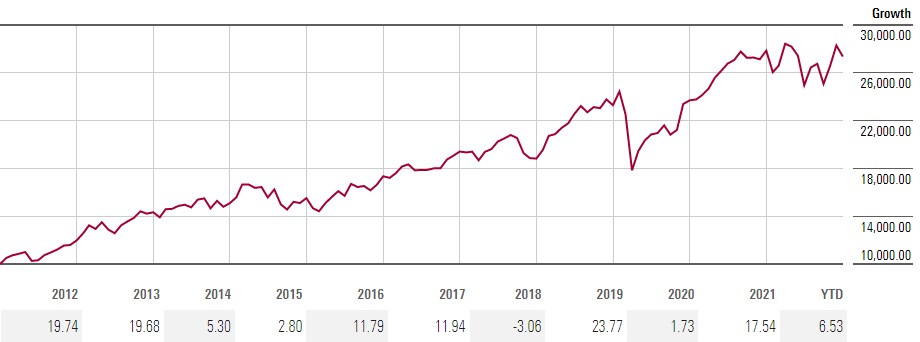

The chart below shows the price movements in the ASX300 for the last 10 years. Offered this same opportunity for the next 10 years until 2033, investors would take confidence in the safety of shares, notwithstanding the losses such as in 2020 when the pandemic hit. On a long-term chart of say 100 years, such losses are hardly noticeable. Investors would prefer a steady return of say 10% each year, but instead, the market gives them this volatility.

Source: Morningstar Investor

Of course, the future is conjecture, and even for investors confident in long-term equity ownership, warnings such as this issued during the week by long-time market bear, Jeremy Grantham of GMO, weigh heavily on the buy decision (the S&P500 is currently about 4,000):

"My calculations of trendline value of the S&P500, adjusted upwards for trendline growth and for expected inflation, is about 3200 by the end of 2023. I believe it is likely (3 to 1) to reach that trend and spend at least some time below it this year or next. Not the end of the world but compared to the Goldilocks pattern of the last 20 years, pretty brutal. And several other strategists now have similar numbers. To spell it out, 3200 would be a decline of just 16.7% for 2023 and with 4% inflation assumed for the year would total a 20% real decline for 2023 – or 40% real from the beginning of 2022. A modest overrun past 3200 would take this entire decline to, say, 45% to 50%, a little less bad than the usual decline of 50% or more from previous similarly extreme levels. But this is just my guess of the most likely outcome."

Little wonder retirees stay conservative with advice such as this on their minds.

If the stockmarket did close for 10 years, investors might learn the advantages of ignoring market values, by:

- Buying stocks which are sure to be around in 10 years, which would reduce short-term speculative plays and focus on top quality companies.

- Increasing the focus on income and dividends as the only place generating money to live on.

- Preventing selling in down markets and encouraging investors to sit on their quality portfolio into the recovery stage.

For anyone who accepts this view but believes it is too late to adopt a multi-decade investment behaviour, here's the oft-quoted Chinese proverb:

"The best time to plant a tree was 20 years ago. The second best time is now."

This is good background to Peter Thornhill's annual update to support the investment approach he has used for over 50 years, to invest in industrial companies paying consistently-rising dividends. Peter argues for ignoring prices and focussing on income, and he updates his main charts and gives 10 sure-fire predictions for 2023.

Inflation and interest rates

The annual inflation rising to 7.8% to the end of 2022 has removed doubts about the Reserve Bank increasing cash rates again in February. Michelle Marquardt, ABS Head of Prices Statistics, said yesterday:

"This is the fourth consecutive quarter to show a rise greater than any seen since the introduction of the Goods and Services Tax (GST) in 2000. The increase for the quarter was slightly higher than the quarterly movements for the September and June quarters last year (both 1.8%)."

Source: Peter Martin

However, on Tuesday, respected RBA watcher, Gareth Aird of CBA, was more focussed on a slowdown in the economy in 2023 including a 'per capita recession' (that is, growth relies on an increasing population). He continued this big call:

"Our economic forecasts are conditional on one final 25bp increase in the cash rate in Q1 23 for a peak this cycle of 3.35%. We believe a higher terminal cash rate is inconsistent with a soft landing. We have 50bp of rate cuts in our profile for Q4 23."

On Wednesday, Aird did not see enough in the new data to change his forecast:

"In the December Board Minutes it was stated that, “the Board is prepared to keep the cash rate unchanged for a period while it assesses the state of the economy and the inflation outlook.”

We continue to see the RBA pausing in their tightening cycle at the March Board meeting. Inflation expectations remain anchored and the recent business surveys suggest that inflation pressures are starting to dissipate, albeit from elevated levels."

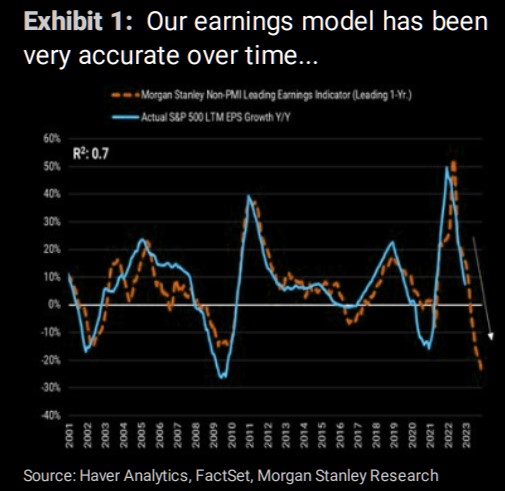

There's more of a fight between the stockmarket bulls and bears than usual at the moment. Wall Street is excited by the possibility of a Fed pivot, where it eases up on interest rate increases. The problem with the interest rate optimism is it misses the other major factor affecting companies: their earnings. This Morgan Stanley chart is a reminder that challenges lie ahead even if central banks stop tightening. The Fed has made it clear it will sacrifice growth to control inflation. The current Fed Funds rate is 4.25% and the CEOs of the big banks such as JP Morgan and Bank of America are saying it will go well over 5% and stay there for all of 2023. That's much higher than companies have seen for many years, and US business and retail indicators are struggling while energy prices are rising again. It's difficult to justify the early 2023 stockmarket optimism.

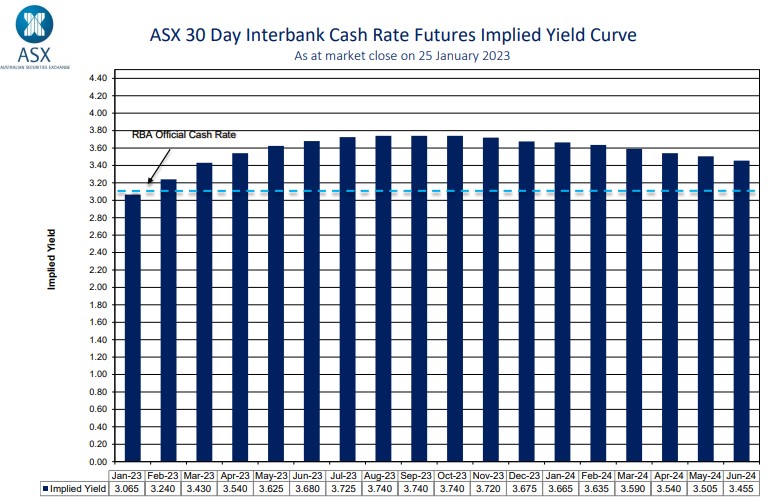

Market expectations for future cash rates, as shown below, are well off their highs although not as low as CBA's forecasts, but they kicked up on Wednesday following the inflation release. There may be some relief for borrowers who were worried about cash rates well over 4% a few months ago.

On the back of the high inflation rates, the Transfer Balance Cap, currently $1.7 million, is set to jump to $1.9 million on 1 July 2023, which also affects the Total Super Balance. Anyone considering starting a superannuation pension soon should take advice on waiting until July, especially as it affects the amount of non-concessional contributions. Remember, the higher limits only apply if you have not yet started a pension.

Two articles from me this week.

First, I gave myself 30 minutes to write an article using Open AI (ChatGPT). I asked it six questions relating to investing and superannuation and the answers were impressive. See what you think, and consider how it might change the future of search and content creation - and maybe my job.

Second, a check of the Annual Morningstar Gameboard for lessons in 20 years of asset class performance. Winners rarely repeat and losers can become winners again, showing the difficulties in forecasting returns.

Also in this week's edition ...

Richard Dinham outlines a new report from Fidelity International that suggests most older Australians are not actively planning for the final chapters of their working life. And critically, the runway to retirement is shorter than expected – most of us don’t work for as long as we intend to.

Meanwhile Doug Drysdale provides a cautionary tale about being the executor of an estate. As an actuary, he expected that being executor of his brother's will would be straightforward, yet it proved anything but. He outlines the traps to avoid.

Julian McCormack of Platinum Asset Management looks at what he considers the world's most important industry, and the least understood: Chinese property. While many investors see it as an asset bubble deflating, Julian believes it's anything but a bubble and represents a compelling opportunity for contrarian investors.

Andrew Macken of Montaka Global Investments is taking a glass-half-full approach to last year's market downturn. He thinks global market leaders in attractive industries are now being priced at multiples far below their intrinsic values. Andrew identifies five ways that investors can position their portfolios for a more optimistic market outlook in 2023.

In the weekend update by Morningstar, Sandy Ward examines Tesla's results and suggests that the stock remains undervalued, while Sarah Dowling says that while Myer announced strong second half sales growth, investors shouldn't get too excited.

In this week's white paper, with increased interest in private debt and prospects for a challenging economic period ahead, Revolution Asset Management asks: is private debt ready for recession?

***

Weekend market update

On Friday in the US, stocks lost altitude late in the session, but still managed another positive finish. The Dow was +0.1%, the S&P +0.3% and the Nasdaq +1%, the latter helped by Tesla surging for a second day, up 11%. Treasurys came under modest pressure with two- and 30-year yields each rising two basis points to 4.19% and 3.64%, respectively. WTI crude slipped below $80 a barrel, gold held at $1,929 per ounce and the VIX settled at 18.5.

From AAP Netdesk: On Friday, Australian shares ended 0.3% higher as sentiment lifted amid a slowing US economy and advances in local financial and technology stocks.

The benchmark S&P/ASX200 index ended 25.5 points, or 0.34%, higher at 7493.8. It touched a fresh nine-month intra-day high of 7508.5 points earlier in the session before settling lower. The index gained 0.2% for the week to record its fourth straight week of gains.

Technology stocks were among the best performers, local technology stocks, with Megaport climbing 7%, and Wisetech, Link Market Services and Xero rising between 1% and 2.5% each.

Heavyweight financial stocks were the other big performers on prospects of expanding margins amid a rising interest rate environment. Each of the Big Four major banks rose between 1% and 1.5%, with CBA closing in on its all-time high of $110.19 a share.

Mining shares were bolstered by strong second-quarter shipments by iron ore exporter Fortescue Metals, with its shares up marginally to $22.49. Bigger rivals BHP and Rio Tinto fared better, lifting about 0.5% each. However, key gold and lithium producers lost ground, with Newcrest Mining down 2.3% while Regis Resources and Pilbara Minerals slid more than 4.0% each.

Coal producers largely contributed to the drop in energy stocks as both Whitehaven and New Hope Corp tumbled 6.6% and 9% respectively. Oil and gas major Woodside also fell 2.4% to $36.42.

From Shane Oliver, AMP:

- Global shares rose over the last week continuing their rally so far this year on signs global inflation has peaked and hopes central banks will become less hawkish and that there will be a soft landing. For the week US shares rose 2.5%, Eurozone shares rose 1.4% and Japanese shares gained 3.1%. Despite worse than expected CPI inflation data and increased market expectations for RBA rate hikes (with the market’s expected cash rate peak this year rising from 3.45% to 3.79%) the Australian share market rose 0.6% for the week, and is now just 1.8% below its all-time high. The $A rose to its highest since June last year.

- The good news over the last week is that global business conditions (PMIs) improved slightly in January and global inflation pressures continue to ease. Europe continues to hold up far better than expected (green line in the next chart) suggesting that it may avoid recession, whereas the US is continuing to run very soft (blue line) suggesting a higher risk of recession there. Overall, the PMIs along with China’s reopening suggest that the risk of global recession has receded a bit.

- The bad news in Australia though is that inflation surprised on the upside again in the December quarter and this is likely to tip the RBA into another 0.25% rate hike in February. Inflation rose to 7.8%yoy, its highest since the March quarter 1990, with key drivers being a surge in holiday travel costs, electricity and new dwellings. While just below the RBA’s forecast for an 8% rise, the further blow out in the trimmed mean measure of underlying inflation to 6.9%yoy (its highest since 1988 against RBA and our own expectations for a rise to 6.5%) is concerning. There is still a strong case for the RBA to pause on rate hikes given the rapid rate hikes to date, to allow for the lagged impact of rate hikes to work and given the risk of unnecessarily knocking the economy into recession. And we think they should pause in February. However, given the stronger than expected rise in underlying inflation in the December quarter, the RBA is likely to want to reinforce its inflation fighting credentials again to keep inflation expectations down particularly given the risks of wages breakout. As a result of this, coming on the back of still strong retail sales we now expect the RBA to raise its cash rate again by another 0.25% at its February meeting.

Graham Hand

Latest updates

PDF version of Firstlinks Newsletter

NEW! Quarterly ETFInvestor (ETF Market Data) from Morningstar

ASX Listed Bond and Hybrid rate sheet from NAB/nabtrade

NEW! In your Interest: listed bonds and hybrids from Bell Potter

LIC Monthly Report from Morningstar