Many investors may be wondering whether there is any value left in Australian fixed income markets. From the perspective of a bond fund manager, compelling risk/return opportunities still allow active managers to provide excess returns.

While outright yields look tight on a historical basis, we contend that select sectors provide attractive risk-adjusted returns relative to cash and government bonds.

Brief Australian debt performance recap

In April 2020, markets bounced quickly in regions such as the US and Europe, where central banks committed to directly supporting credit markets. However, in Australia the Reserve Bank of Australia (RBA) fell short of this commitment and conditions remained challenged, although they eased somewhat in May following the RBA’s easing of collateral lending terms.

Turn the clock forward to September. Yields on senior bank debt for the major banks are now trading at low levels not seen since prior to the GFC. Support for domestic credit markets continues to expand as debt issuance by corporations receives strong demand. A record low cash rate drives investors toward non-government debt in a search for yield, improving liquidity markedly.

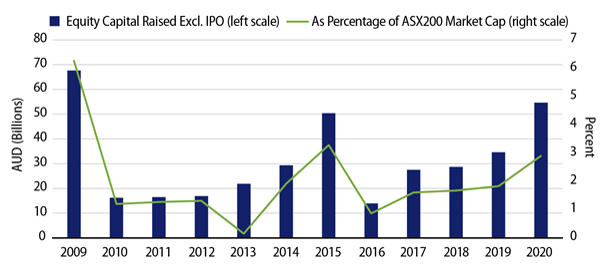

Corporate treasurers have also acted decisively to mitigate the impacts of the virus on their balance sheets. Businesses raised liquidity to allow themselves to survive the forced shutdown of the economy. Most companies tapped lines of bank credit, and many listed companies issued equity at levels not seen since the GFC (for example, BEN, NAB, NSR, NXT, QBE, QAN and more), as shown below. Dividends were suspended and costs aggressively cut across the board in order to preserve cash. While slow to start, a growing number of Australian companies are issuing into the debt markets.

Exhibit 1: Equity raisings by Australian companies

Source: Capital IQ, Bloomberg. As of 30 June 2020.

Looking for value across the banking capital structure

A combination of ongoing access to the term funding facility (TFF) and anaemic loan growth have left the banks with significant liquidity and little need to issue new senior debt to fund loan growth. In fact, banks have not needed to issue senior debt since the onset of the crisis, with maturing bonds not being refinanced. The RBA has advised:

"The TFF provides a source of low-cost funding for the banking system, with funding available for three year terms at a fixed interest rate of 0.25%. This helps to support the supply of credit and lower interest rates for households and businesses."

By 1 September 2020, drawing under the TFF reached $52 billion.

Bank debt issuance usually provides the bulk of investment opportunities in domestic credit markets, and with supply falling, the scarcity value of the outstanding bonds increases. As a result, the low bank yields are not likely to reverse any time soon.

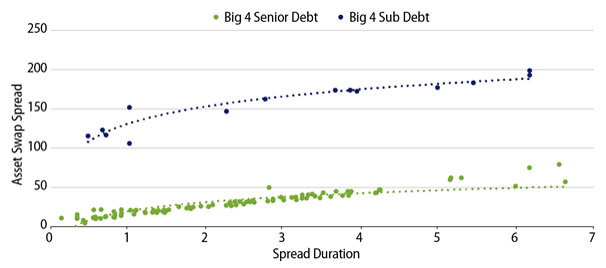

Banks issue debt across the capital structure, including senior and subordinated debt, alongside hybrid (AT1) capital. While senior debt has repriced to levels not seen since before the GFC, valuations of bank subordinated debt have not retraced to the same extent.

With the capital position of the domestic banks remaining sound, and ongoing support being in place, we feel that subordinated debt has some room to appreciate in value, and remains the more attractive part of the capital structure to invest in.

Exhibit 2: Major bank sub debt offers value

Source: Bloomberg, Western Asset. As of 2 June 2020.

Potential opportunities in Residential Mortgage Backed Securities

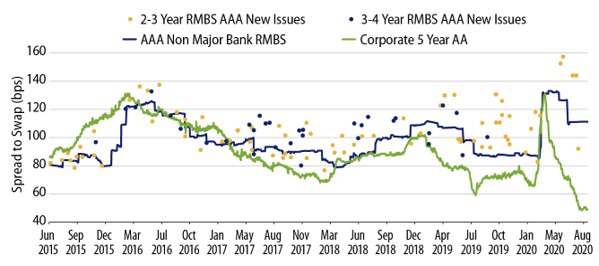

Another sector that has benefitted from the current mix of policies is the domestic Residential Mortgage Backed Securities (RMBS) sector. While lockdowns have led to an increase in the number of households unable to meet their monthly payment commitments, the flow-on effects have been mitigated due to significant regulatory intervention.

The Government has acted swiftly to limit the impact of COVID-related arrears on the performance of both home loan providers and the RMBS bonds that they issue. The aim is to avoiding the type of dislocation experienced during the GFC, when the valuations on RMBS blew out significantly worse than corporate credit.

Direct purchasing of RMBS by the Structured Finance Support Fund (SFSF) and the establishment of the SFSF Forbearance Fund, which is designed to assist non-bank lenders to cover payment shortfalls on loans affected by COVID-19, have led to the RMBS sector being well supported and have reduced the stresses on RMBS structures. This support has allowed lenders to maintain access to funding and focus on assisting borrowers to manage their way through the crisis, rather than forcing foreclosures on affected borrowers.

In April, we saw the average level of loans in partial or full forbearance rise sharply to around 10% for prime loans and near 20% for non-conforming loans. Encouragingly, we are seeing signs that the sector is repairing as the economy heals, and these forbearance numbers have tracked downward.

Unless the stresses increase significantly from here, we expect the structures to remain robust and therefore expect RMBS to perform well. RMBS yields, like those of bank-subordinated debt, are likely to continue to offer significant value for patient investors.

Exhibit 3: Australian RMBS vs. major bank senior bonds

Source: Bloomberg. As of 31 May 2020.

Foreign issuer AUD debt issuance

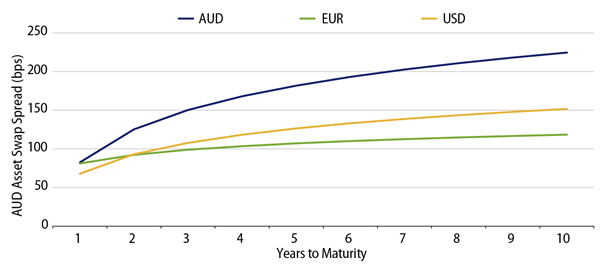

An additional area of opportunity exists in the form of bonds of offshore issuers. These companies primarily issue into the Australian market to diversify their sources of capital, provide a natural hedge for AUD-denominated earnings and for tax efficiency.

Such bonds are commonly referred to as Kangaroo bonds. There are currently many Kangaroo issuers where the AUD-denominated bonds are much cheaper (yields higher) than the issuers’ USD- and EUR-denominated bonds. Both the Fed and ECB are explicitly supporting credit markets via their asset purchasing programs. This has acted to significantly reduce the yields on eligible bonds. No such direct policy exists in Australia, leaving the AUD bonds undervalued in comparison to global peers.

The longer markets remain flush with liquidity in a yield-starved environment, the greater the likelihood that the yields on bonds issued across all currencies will converge. This presents a compelling opportunity for managers with a global research platform to build early conviction in the most robust Kangaroo names.

Exhibit 4: Foreign Issuer AUD Denominated Bonds Trading Wide of Global Curves*

Source: Bloomberg. *A rated issuance from euro bank issuers. As of 30 Jun 2020.

We are not out of the woods yet, in terms of either the health or the economic consequences of COVID-19. However, a combination of aggressive monetary, fiscal and regulatory actions has provided the much-needed support to the economy. This unprecedented level of support does not reduce the need for intensive fundamental analysis. Indeed, it makes such research even more important.

The dislocations caused by selective government support and increased uncertainty within certain sectors does provide what we feel are compelling risk/return opportunities for active bond fund managers across segments of the market.

Jonathan Baird is a Product Specialist and Damon Shinnick is a Portfolio Manager and Senior Research Analyst for Western Asset Management, a Franklin Templeton specialist investment manager. This article is for information purposes only and reflects the current opinions of Western Asset Management. It has been prepared without taking into account the objectives, financial situation or needs of any individual.

Franklin Templeton is a sponsor of Firstlinks. For more articles and papers from Franklin Templeton and specialist investment managers, please click here.