The Weekend Edition includes a market update plus Morningstar adds links to two highlights from the week.

Weekend market update

On Friday in the US, markets surged with the S&P500 up 1.9% and the NASDAQ gaining 1.8%.

From AAP Netdesk: The Australian sharemarket closed lower on Friday after iron ore prices tumbled to a 10-month nadir on demand fears from China.

After falling by 113 points, or 1.7%, in the first 45 minutes of trading, the benchmark S&P/ASX200 index climbed steadily to finish the day down 45 points, or 0.7%. The mining sector dropped 3.2% on the day to finish the week down 6.1%, its sixth consecutive week of declines.

Chinese economic data released at midday Friday showing the world's second-largest economy grew just 0.4% in the second quarter, well below expectations. Rio Tinto finished down 2.9% after the miner reported that skilled labour shortages and inflation had hit its second-quarter earnings. BHP and Fortescue likewise hit their lowest level this year, 3.5% and 6.2% respectively. Goldminers Newcrest, Northern Star and Evolution were all down, hitting multi-year lows.

ANZ fell 1.3% to $21.64, Macquarie dropped 1.8% to $167.99 and Westpac dipped 0.2% to $19.90. CBA was flat and NAB rose 0.5% to $28.45. Pendal Group was down 7.8% to a nine-year low of $3.76 after the fund manager announced funds under management dropped to $111 billion in the June quarter, from $124.9 billion.

From Shane Oliver, AMP Capital: Share markets mostly fell over the last week on fears that still rising inflation will trigger faster rate hikes and recession. While Japanese shares rose, US, European and Chinese shares fell although a Friday rally moderated US losses. The fall in Eurozone shares was magnified by the risk of a permanent shutdown of Russian gas flowing through the Nordstream 1 pipeline to Germany.

Inflation and interest rate hikes, and the fear they will drive recession, continued to dominate investment markets. However, headline inflation is likely to slow in July helped by a sharp fall in gasoline prices and falling upstream price pressures. But for now, the Fed will remain aggressive, seeking to slow demand and cool the labour market which is likely contributing the ongoing acceleration in services inflation. We expect the Fed to hike again by 0.75% later this month but there is a high risk that it will hike by 1.00%. This increases the risk that the Fed goes too far knocking the US economy into recession.

***

'Cakeism' was shortlisted for the Oxford English Dictionary word of the year in 2018 and is undergoing a revival. The language is always evolving, with new words entering our lexicon regularly. Cakeism comes from 'having your cake and eating it too', but the word now means variously 'a wish to enjoy two desirable but incompatible alternatives' or 'proposing a future scenario that sounds better than is actually achieveable'. Enter the Reserve Bank and Governor Philip Lowe. They want to simultaneously fight inflation by taking away spending power while not creating a slowdown that pushes into a recession. The massive injection of government money and central bank stimulus helped cause the inflation which is now hitting the same people the money was supposed to assist.

And here's the dilemma for investors:

"Recession talk cannot seriously be applied to Australia. Westpac continues to forecast Australia's economy to grow 4% over 2022, led by consumer spending pent-up from Covid lockdowns into early 2022." Sean Callow, Westpac.

“Recession or not, the next 12-18 months is going to feel like one, especially for equity investors.” Raheel Siddiqui, Neuberger Berman

One of the reasons the Governor is speaking regularly at public and media events is his desire to talk down consumer optimism. Confidence is usually a good thing, but it is proving a headache for the Reserve Bank, as low unemployment and government assistance have encouraged consumers to spend.

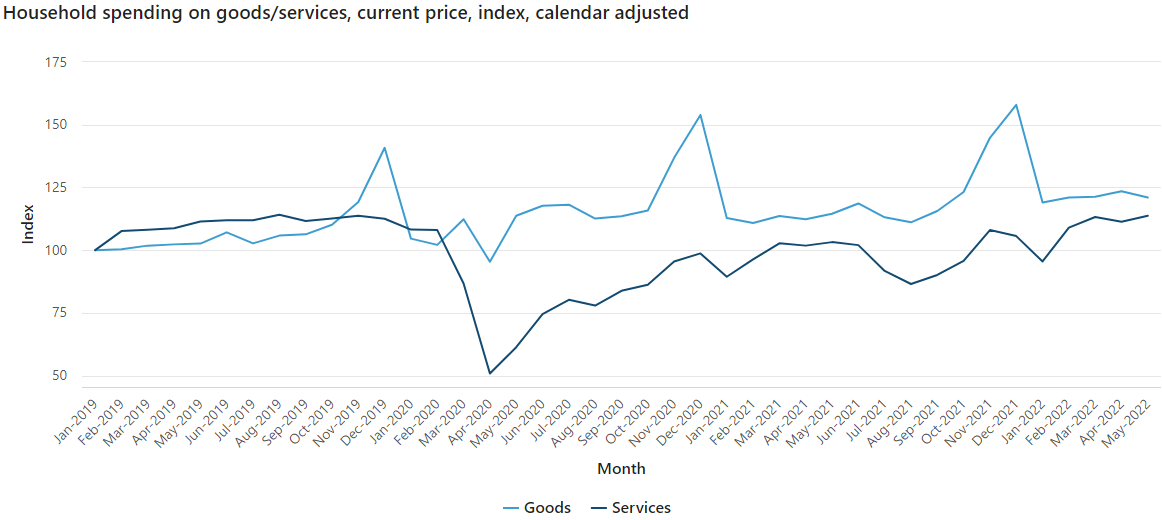

This week, the ABS released the latest household spending for May 2022, showing a rise of 7.9% compared with the same time last year. Jacqui Vitas, Head of Macroeconomic Statistics, said household spending increased in all categories:

“Strength in the services categories was driven by transport (up 14.5%), as air travel continued to recover, and higher petrol prices increased motor vehicle running costs. Strong growth was also seen in spending on miscellaneous goods and services (up 12.6%), hotels cafes and restaurants (up 10.3%), and recreation and culture (up 10.0 per cent)."

Compared to pre-pandemic January 2020, total household spending is 10% cent higher in current prices. The Reserve Bank started increasing cash rates on 4 May, but only by 0.25%, so perhaps the message had not reached enough people.

While this spending pushes Philip Lowe to raise rates, other indicators of consumer sentiment provide reason for the Reserve Bank to temper its new enthusiasm for rate rises.

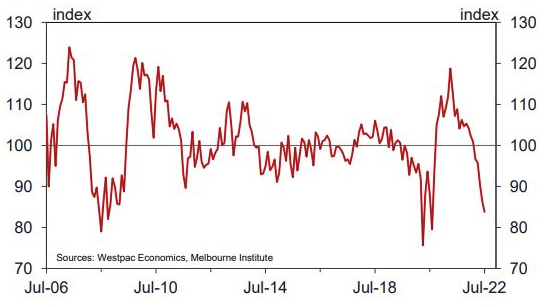

The Westpac-Melbourne Institute index of consumer sentiment is falling sharply, and is now at levels only seen during major disruptions. Consumer confidence is hit by economic events, such as the GFC and Federal Budgets, and of course, it took a severe hit in 2020 during the pandemic before recovering on vaccine optimism. It has now fallen for seven months.

Consumer Sentiment Index

What is the relevance of all this for interest rates? As Westpac says:

"The cash rate has increased at a faster pace than we have seen in any cycle since 1994 and this is clearly unsettling for consumers also facing a sharp rise in the cost of living. A more cautious approach will be appropriate once policy has moved to ‘neutral’ in August."

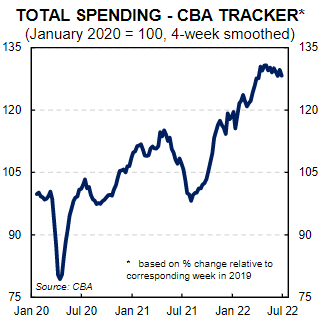

More up-to-date data is provided by the CBA Tracker:

"Our internal CBA credit and debit card spending data to 8 July has been showing a clear decline in the pace of spending growth. The falls have also been more noticeable in some of the discretionary spending categories that households are likely to pull back on first. With prices continuing to increase, that indicates the volume of consumer spending is likely to be even softer."

Back to cakeism. Perhaps Philip Lowe will enjoy a rich black forest rather than a simple sponge if consumer sentiment falls enough to stop him increasing rates toward the predicted 3% or even 4%. Thousands of borrowers will celebrate if he has his cake and eats it too. If borrowers want to help, they should stop buying stuff.

Hopes for inflation easing were not helped on Wednesday night when US consumer prices rose 9.1% in June 2022 from a year ago, above expectations. It's a 40-year-high driven by increases in gas, food and rent. The US market is now pricing in another 1% rise from the Federal Reserve later this month.

Which is all feeding into the ways Australians are investing, and three recent reports show the latest funds flows locally as well as globally. Compared with 2021, Australians have significantly changed how they are investing in 2022.

Another factor which is suddenly playing into the Reserve Bank thinking is the potential impact of a new Covid wave. I had my fourth jab on Monday, the first day it was available to under 65s, and I'm surprised how many people do not wear masks on public transport. I was in a lift on Monday where people piled in like the old days. We have become too relaxed. The implications stepped up this week when Federal Health Minister Mark Butler said Australians should consider working from home to curb rising Covid-19 cases. He said millions of Australians may be infected in the last six weeks of winter.

It's time to pay serious attention to pandemic again. The latest subvariant easily overcomes immunity from prior infections and vaccines and increases the risk of reinfection. The same variant is taking hold in the US and China, and may go some of the way to slowing the economy instead of central bank tightening. Adrian Esterman checks the evidence and numbers.

Firstlinks has covered the banning of stamping fees paid to brokers and financial advisers in great detail, such as here and here. Treasury is undergoing a post-implementation review of this 2020 policy, and we have gained access to the full submission by the Australian Shareholders' Association's Rachel Waterhouse. It seems unlikely the policy will change, with Stephen Jones, Minister for Financial Services telling The Australian Financial Review:

“I will look at the report, but it would be an extremely high bar to get over. I am focused on more Australians getting access to quality advice, not opening up the door to conflicted remuneration again.”

I'm with Jones on this one as there was plenty of evidence that brokers and advisers placed clients into funds based on receiving the fee. How else could a relatively unknown fund manager raise a billion dollars in a month?

We welcome the return of veteran global pension consultant, Don Ezra, who gives an intriguing explanation of how our lives will change when living to 100 is normal. He sees a good life lived in five acts.

Ashley Owen shares one of his great slides to show what has happened to Australian house prices over decades of inflation, and yes, real price falls are common. The 40% increase in 2020 to 2021 was extraordinary and we are now paying for the stimulus largesse, but buying a home is a long-term decision and favourable fundamentals are still in play.

We tend to focus on averages when describing markets, such as the market went up 'x%' or recessions usually last 'y days'. Robert Almeida warns that averages provide no insights into variations, and the peaks and troughs that can really damage a portfolio. Every market cycle or recession is different.

Some investors argue firmly for an allocation to gold, but others criticise it for the lack of income and price volatility. Sawan Tanna identifies five major misconceptions in making the case for gold in a diversified portfolio.

This week, Morningstar looked at opportunities in a down market with Susan Dziubinski checking 33 undervalued opportunities in US shares and Vikram Barhat discusses three cloud-based companies to counter recession fears.

Even if you don't usually read our White Papers, this week's from Neuberger Berman is well worth a look. Reporting on the Q3 meeting of their Asset Allocation Committee, they explain the rationale for making multi-sector portfolio adjustments like this:

In brief, more into quality bonds to earn higher yields, less into equities to avoid a possible earnings downgrade.

Graham Hand

A full PDF version of this week’s newsletter articles will be loaded into this editorial on our website by midday.

Latest updates

PDF version of Firstlinks Newsletter

IAM Capital Markets' Weekly Market Insight

ASX Listed Bond and Hybrid rate sheet from NAB/nabtrade

Monthly market update on listed bonds and hybrids from ASX

Indicative Listed Investment Company (LIC) NTA Report from Bell Potter

Monthly Investment Products update from ASX

Plus updates and announcements on the Sponsor Noticeboard on our website