The Weekend Edition includes a market update plus Morningstar adds links to two highlights from the week.

Weekend market update

On Friday in the US, the S&P500 added another 1.4% while NASDAQ was even stronger, up 1.9%.

From Shane Oliver, AMP: The bounce back in shares continued over the last week on hopes that slowing growth will see central banks ease up on the pace of monetary tightening helped along by mostly good earnings results, despite stronger than expected US and European inflation data. For the week US shares rose 4.5% and Eurozone shares gained 3% but Japanese shares fell 0.4% and Chinese shares lost 1.6%.

The rally since the June lows has been lacking in conviction. We need to see clearer signs that inflation has peaked such that central banks can slow and then stop raising rates and it's still early days in the profit downgrade cycle. On a 6-12 month horizon we remain optimistic on shares as inflation recedes, central banks become less hawkish and a deep recession is likely to be avoided, but there is a way to go yet.

From AAP Netdesk: The benchmark S&P/ASX200 index closed on Friday up 55 points, or 0.8%, and finished the week up 2.3% and closed out July up 5.7% to an almost seven-week high in its best monthly performance since March and second-best in the past year-and-a-half. The gains this Thursday and Friday followed the release of second-quarter Australian inflation data that was milder than expected, as well as suggestions the US Federal Reserve would take a break from its aggressive monetary tightening campaign.

Property was the best performer on Friday, up 2.9% as Goodman Group rose 4.6% and Vicinity Centres climbed 2.5%. The heavyweight mining sector climbed 1% and all the big banks were higher. CSL fell 0.5% to $289.84 as the Aussie dollar gained ground against the weakening US dollar, the currency in which the blood products giant makes much of its money. Origin Energy gained 4.2% after the energy giant reported that full-year revenue from its Australia Pacific LNG joint venture.

A phenomenal three-day rally by buy now, pay later companies finally ran out of steam, with Zip falling 25%, Sezzle down 19.6% and Laybuy retreating 23%. That leaves those companies with an excellent weekly performance - Sezzle up 173% and Laybuy up 150% - although of course they're also still very much off their highs from 2021.

***

There is another side to the surge in inflation that deserves far more attention. When inflation was close to zero, and the central bank fear was deflation, it was not so important to think about markets and returns in real terms, that is, nominal returns less inflation. If inflation is zero and stock prices rise 5%, that's a 5% real return. But with Australian inflation now at 6.1% and perhaps heading to 7% according to the Reserve Bank, US inflation already at 9% and the UK above 10%, investors need to think in real terms. A total nominal return of say 6% including dividends may represent a real return of zero.

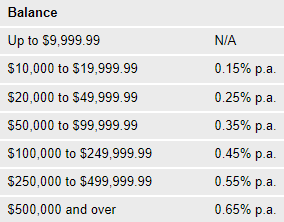

There are many consequences for investing. At zero inflation, it did not matter as much if money was left in a bank account earning little or no income. But if inflation is 6% to 7%, significant purchasing power and living standards are being eroded. The table below shows the interest rates currently paid on my SMSF's main transaction account where I leave a decent amount of cash. My bank has passed on a fraction of the cash rate rises.

The yield curve is now steep so the opportunity cost of leaving money in the cash account versus term deposits, notes or bonds is far higher than for many years, depending on the alternative. This week, for example, I deployed some cash into a new NAB subordinated issue paying around 6.3% with an issuer call in 2027. Yes, I am accepting fixed rate risk and credit risk on NAB but I'm also 6% ahead of current cash rates. Although cash will continue to rise, my bank will not pass on the full increase.

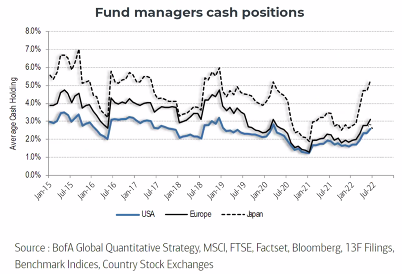

Retail investors holding cash are not alone. According to the latest survey from Bank of America, cash holdings in fund managers portfolios in major global centres have risen over 2022 and although not historically high (holdings in equities still dominate), they are the highest level for over two years.

Another side of inflation rising above 6% is that many social security payments or regulatory limits linked to CPI which moved slowly in the past will now rise rapidly (in nominal terms). Examples are pensions, usually linked to six-monthly changes in CPI, and superannuation limits. The Transfer Balance Cap (TBC) increased for the first time to $1.7 million on 1 July 2021, but an additional 6% is $102,000, which might mean the next increase up to $1.8 million comes a lot quicker. Is this enough for someone to delay opening their first retirement income stream until after 1 July 2023 to obtain a personal TBC at the higher level?

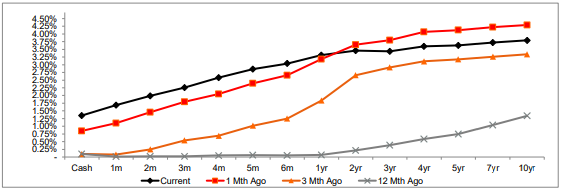

With rising rates in our minds, many people do not realise that longer-term fixed rates have already fallen in the last month. The bank swap yield curve chart below, sourced from NAB, shows the current (as at 26 July 2022) 10 year (the black line) at 3.8% but it was 4.3% a month ago (the red line) and 3.3% three months ago (the orange line). Maybe investors have missed the rate top a few weeks ago (when we published this article on the choices) but it's volatile and rates may yet go higher (although for this weekend update, note that long-term rates continued to fall for the rest of the week).

At some point, like on the NAB issue, investors have to accept the deal on the day it is available. My opinion is that 6.3% fixed on NAB for five years has a place in my diversified portfolio but NAB also offered a floater at 3 month BBSW+2.8%. As a sign of demand, NAB received bids for $2.4 billion in a couple of days and printed $250 million of the floaters and $1 billion of the fixed. NAB is indifferent but investors voted with their wallets.

The chart also shows how much the yield curve has flattened and this is significant. Someone tried to convince me during the week that if the cash rate continues to rise, so will the long bond rate. Maybe, but it doesn't usually work like that. Rising cash signals Reserve Bank determination to bring inflation under control, and that is why the long-end rates have fallen. The market is saying central banks around the world will tame inflation relatively soon.

Here is the view of Russel Chesler of VanEck after the ABS released the latest quarterly CPI data on Wednesday:

"The CPI rose 1.8% in the June 2022 quarter, to be 6.1% higher from a year ago. The stock market rose on the news, as inflation in the second quarter dipped from the first quarter and was slightly lower than expected. Inflation in Australia may have already peaked with the fall in quarterly inflation from 2.1% to 1.8%. Recent falls in the prices of wheat and corn are likely to slow food inflation, which accelerated over the last quarter ... VanEck expects further increases bringing official rates to 2.75% by the year's end, which will place significant upward pressure on mortgage lending rates."

Meanwhile, last night the US Fed raised its rate by 0.75% to 2.25%-2.50% but suggested the next increase could be smaller. The Fed said that although “inflation remains elevated”, “recent indicators of spending and production have softened” but “anticipates that ongoing increases in the target range will be appropriate.” The stockmarket liked it and the S&P500 rose 2.6% with the rate-sensitive NASDAQ up 4%. Although bond rates were little changed, there is more hope that inflation will be managed without significant economic impact.

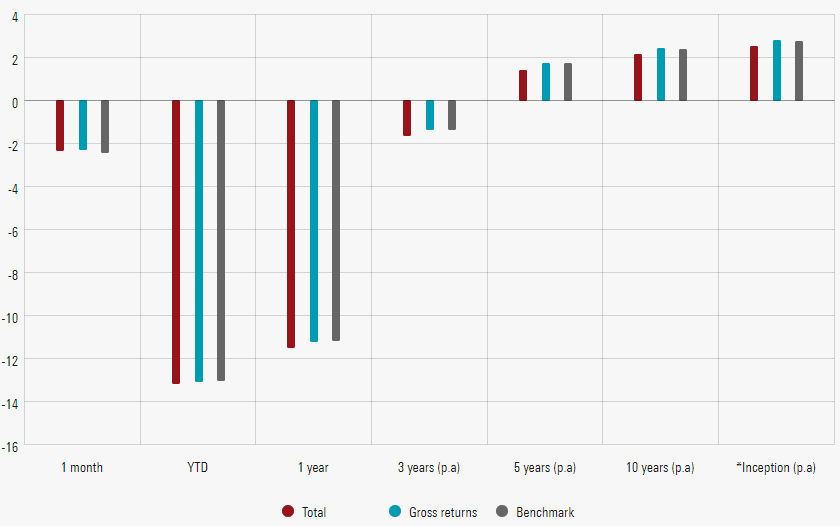

In fact, the US market is now pricing in a switch from rising to easing rates from mid 2023. A good example in Australia of inflation expectations is shown in the prices of inflation-linked bonds. Intuitively, an investor might expect high demand for these bonds as the yield rises with inflation. Yet, as shown below, the Australian index of such bonds has lost 13% YTD. Investors see the inflation spike as temporary, and as the Vanguard fund has a weighted average maturity of nearly 10 years, the market focus is on the long term.

Vanguard Australian Inflation-Linked Index Fund, returns

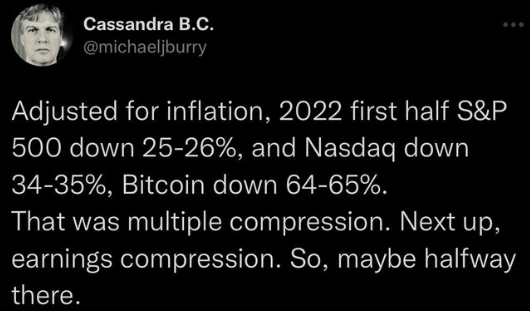

Back to adjusting our thinking for inflation, this tweet from Michael Burry (the guy featured in The Big Short who made millions buying credit default swaps before the GFC) reminds us that share prices should also be adjusted for inflation. If your portfolio is down 20% in nominal terms and inflation is 5%, your money has lost 25% of its purchasing power. And by the way, Burry believes the market has much further to fall because all we have seen so far is a shrinking (compression) in Price to Earnings ratios, not the consequences of a fall (compression) in earnings.

Finally, some thoughts on the strength of the Australian consumer and recent company results from Johannes Faul, Director of Equity Research at Morningstar.

"So, we've been very surprised on how strong the consumer is in Australia in terms of their spending. So, JB Hi-Fi surprised us significantly on the upside on their sales in the fourth quarter, in the June quarter. And then, today, Myer announced very strong sales results on top of already strong sales in the previous corresponding period. So, everything is pointing towards the Australian consumer has been still buying TVs and apparel in the June quarter and into July. But we see that shifting. We see the warning signs that we're seeing in the US, just like everyone else, and we think the writing is on the wall. And what's really happening is, if you think about the momentum where that's going to head is, we have record low unemployment. We've got very low interest rates that are now sharply going up. We have a lot of savings that are on the sidelines. So, we are almost in the perfect position, but the momentum we see is going backwards and that spells trouble for earnings in the consumer discretionary market, so thinking JB Hi-Fi, Harvey Norman, Myer, those stocks will see earnings weaken going into fiscal 2023 on our numbers."

In this week's edition ...

The most-used standard for deciding how much money and income is needed in retirement has been the ASFA Standards for many years, but there is now a rival from Super Consumers Australia (SCA). Claiming ASFA numbers are too high due to a bias towards superannuation, SCA estimates the amount required is significantly lower. Do you agree?

As investors look for better signs to commit more to equities, we have two articles reminding us that the sharemarket is not the economy. Our interview with Anthony Aboud of Perpetual includes his thoughts on the leading indicators he looks for and stocks he likes at the moment, while Andrew Mitchell says investors should not equate bear markets with recessions as he describes a range of historical patterns.

Hugh Selby-Smith argues that price is not a scientific measure but is better described as a liar, and he offers three steps for those who want to invest in the current tough markets.

When people think about EVs, attention turns to cars or commodities, the Teslas and the lithiums. But Kate Turner and Peter Meany check a sector which has done relatively well this year, infrastructure. There should be more focus on the 'E', as all these 'Vs' will need charging.

A recent High Court decision has ruled on lapsing binding death benefit nominations for SMSFs, and Julie Steed looks at the implications. Part of the responsibility of being an SMSF trustee is staying aware of the rules.

Given the importance of bank lending and interest rates for our economy, Stephen Wu gives a quick take in six charts summarising the dramatic changes in lending in only six months. Hard to believe it was as recently as the start of 2022 when central banks believed inflation was not a threat.

In highlights from Morningstar this week, Lauren Solberg shows the bounce by tech stocks since 16 June and asks if it is fickle or firm, while Nicki Bourlioufas checks with analysts on their revisions to mining stock values as commodity prices fall.

This week's White Paper from Vanguard highlights the major economic and market developments expected for the rest of calendar 2022.

Graham Hand

Latest updates

PDF version of Firstlinks Newsletter

Australian Ethical webinar series:

Part 1 - Investing in the Australian equity market in 2022 10 August 2022.

Part 2 - A wrap-up of recent advocacy and engagement activities 23 August 2022.

IAM Capital Markets' Weekly Market Insight

ASX Listed Bond and Hybrid rate sheet from NAB/nabtrade

Indicative Listed Investment Company (LIC) NTA Report from Bell Potter

LIC Monthly Report from Morningstar

Monthly Funds Report from Cboe Australia

Plus updates and announcements on the Sponsor Noticeboard on our website