It seems momentous things happen in years ending in seven. Starting with the ‘summer of love’ in 1967 and the introduction of the Chevrolet Camaro. After that, it was downhill with Elvis leaving the building in 1977, the 1987 share market crash, the Asian crisis of 1997 and the GFC in 2007. While Lehman Brothers didn’t go bankrupt until September 2008, the GFC’s initial tremors occurred in 2007, with shares taking a hit in August before rebounding to new highs in the US and Australia in October and November 2007 ahead of a roughly 55% decline into March 2009. What are the main lessons for investors from the GFC and can it happen again?

What drove the GFC?

The GFC was the worst financial crisis since the Great Depression. It saw the freezing up of lending between banks, multiple financial institutions needing to be rescued, 50% plus share market falls and the worst post-war global economic contraction. Too many loans to US homebuyers set off a housing boom that went bust when interest rates rose and supply surged. No big deal – it happens all the time! But it was what went on around it that ultimately saw it turn into a global crisis.

- A massive proportion of the loans (40% or so) went to people who had no ability to service them, such as sub-prime and low doc borrowers. Remember NINJA loans – loans to people who had no income, no job and no assets! And many were non-recourse loans, so borrowers could just hand over the house if its value fell below the debt owed and that was the end of their liability. Recall – jingle mail!

- This was encouraged by public policy aimed at boosting home ownership and ending discrimination in lending.

- It was made possible by a massive easing in lending standards facilitated by financial innovation that packaged up the sub-prime loans into securities, which were then given AAA ratings on the basis that while a small proportion of loans may default the risk will be offset by the broad exposure. But the trouble was that with the sub-prime loans moved out of the banks, there was no ‘bank manager’ looking after them.

- This all came as banks globally were sourcing an increasing amount of the money they were lending from global money markets – which had freed them up from relying on expensive bank deposits via bricks and mortar branches.

The music stopped in 2006

Poor affordability, an oversupply of homes and 17 interest rates hikes from the Fed over two years saw US house prices peak and then start to slide. This made it harder for sub-prime borrowers to refinance their loans at their initial ‘teaser’ rates. The problem caught the attention of global investors in August 2007 after BNP froze redemptions from three of its funds because it couldn’t value the Collateralised Debt Obligations (CDOs), which in turn set in train a credit crunch. The global economy fell into recession, mortgage defaults escalated and multiple banks failed.

The crisis went global as losses mounted, magnified by gearing, which forced investment banks and hedge funds to liquidate sound positions to meet redemptions thereby spreading the crisis to other assets. The distribution of securities globally led to a wide range of exposed investors and hence greater worries about who was at risk, which all affected confidence and economic activity.

Fault lay with home borrowers, the US Government, lenders, ratings agencies, regulators, and investors and financial organisations for taking on too much risk.

It came to an end in 2009 after significant monetary easing and fiscal stimulus helped restore the normal operation of money markets, confidence and growth. That said, aftershocks continued with sub-par global growth and very low inflation.

Lessons from the GFC and its aftermath

The GFC highlighted several lessons for investors:

- The economic and investment cycle is alive and well. Talk of a ‘great moderation’ was all the rage prior to the GFC but the GFC reminded us yet again that periods of great returns are invariably followed by a fall back. If returns are too good to be true they probably are.

- High returns come with higher risk. While risk is often dormant for years, it usually returns with a vengeance as was apparent in the GFC. Backward-looking measures of volatility are no better than attempting to drive focussed only on the rear-view mirror.

- While each boom bust cycle is different, markets are pushed to extremes of valuation and sentiment. The low in 2009 was characterised by ultra-cheap shares and credit investments with investors highly pessimistic.

- Be sceptical of financial engineering or hard-to-understand products. The biggest losses for investors in the GFC were generally in products that relied heavily on financial engineering purporting to turn junk into AAA investments that were impossible to understand.

- Avoid too much gearing or gearing of the wrong sort. Gearing is fine when all is going well. But it will magnify losses when things reverse and can force the closure of positions at a big loss when the lenders lose their confidence or when margin calls force investors to sell their position just at the time they should be adding to it.

- The importance of true diversification. While listed property trusts and hedge funds were popular alternatives to low-yielding government bonds prior to the GFC, through the crisis they ran into big trouble (in fact Australian Real Estate Investment Trusts (REITs) fell 79%), whereas government bonds were the star performers. REITs have since cut their gearing and returned to their knitting.

- Fiscal and monetary policy work. There is a role for government in putting free market economies back on track when they get into a downward spiral. While some have argued that easy money just benefitted the rich (who invest in shares), doing nothing would have likely ended with 20% plus unemployment and worse inequality.

- The return to normal from major financial crises can take time, as the blow to confidence depresses lending and borrowing and hence consumer spending and investment for years afterwards. This muscle memory eventually fades but the impact can be seen for a decade or so.

- The importance of asset allocation. What really matters for your investment performance is your asset mix – ie your allocation to shares, bonds, cash, property, etc. Exposure to individual shares or fund managers is second order.

- Finally, ‘stuff happens’. While after each economic crisis there is a desire to ‘make sure it never happens again’, history tells us that manias, panics and crashes are part and parcel of the process of ‘creative destruction’ that has led to an exponential increase in material prosperity in capitalist countries. The trick is to ensure that the regulation of financial markets minimises the economic fallout that can occur when free markets go astray but doesn’t stop the dynamism necessary for economic prosperity.

Will it happen again?

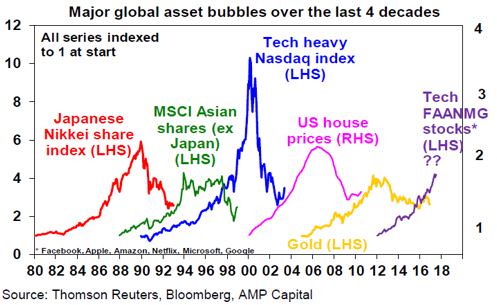

Of course, there will be another boom and bust but the specifics will be different next time. History is replete with bubbles and crashes and tells us it’s inevitable as each generation forgets and must relearn the lessons of the past. Often the seeds for each new bubble are sown in the ashes of the former. Fortunately, in the post-GFC environment seen so far there has been an absence of broad-based bubbles on the scale of the tech boom or US housing/credit boom. E-commerce stocks like Facebook and Amazon are candidates but they have seen nowhere near the gains or infinite PEs seen in the late 1990s tech boom.

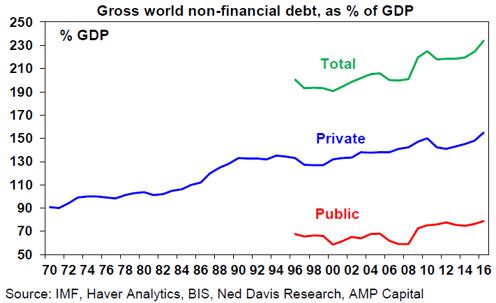

Global debt has grown to an all-time high relative to global GDP.

However, high debt does not mean a crisis is upon us. It has been trending up for decades and much of the debt growth in developed countries post GFC has been in public debt and debt interest burdens are low thanks to low interest rates.

Furthermore, the other signs of excess that normally set the scene for recessions and associated deep bear markets in shares are not present on a widespread basis just now. Inflation is low, monetary policy globally has barely tightened, there has been no widespread over-investment in technology (as preceded the tech wreck) or housing (as preceded the GFC in the US) and bank lending standards have not been relaxed to the same degree as seen prior to the GFC. Moreover, financial regulations have tightened significantly with banks required to have higher capital ratios and source a greater proportion of funds from their depositors.

While another boom bust cycle is inevitable at some point, many of the signs of excess that normally precede deep bear markets are still absent.

Dr Shane Oliver is Head of Investment Strategy and Chief Economist at AMP Capital. This article is general information and does not consider the circumstances of any investor.