The Weekend Edition includes a market update (after the editorial) plus Morningstar adds links to two additional articles.

Mark it in your diary. In a few weeks, on 9 May 2023 at 7.30pm, Treasurer Jim Chalmers will deliver the Federal Budget for 2023/24. Last year, an earlier 'election budget' was presented in April by Josh Frydenberg, and then Chalmers handed down a light interim Budget in October 2022. The next one will be more substantial, delivered by a Treasurer who has signalled his time in office will not be wasted. His recent essay in The Monthly on 'values-based capitalism' defined his core mission to:

“redefine and reform our economy and institutions in ways that make our people and communities more resilient, and our society and democracy stronger as well”.

But it was more than this. He quoted a Greek philosopher, Heraclitus:

“No man ever steps in the same river twice. For it’s not the same river, and he’s not the same man.”

He wants to set the stage for major changes, although the more politically-pragmatic Prime Minister may curb his enthusiasm. Recent attempts at reform by Labor politicians have not ended well. It will be the biggest day of the Treasurer's career and he is no stranger to the process. He has worked on or responded to 16 budgets in government and opposition, and in The Monthly, he specified three objectives:

"First, an orderly energy and climate transition ...

Second, a more resilient and adaptable economy in the face of climate, geopolitical and cyber risks, unreliable supply chains, and pressures on budgets from an ageing population.

Third, growth that puts equality and equal opportunity at the centre."

Changes such as the new tax on super balances over $3 million will be joined by other policies. We have already seen a windback in the LMITO (Low and Middle Income Tax Offset), worth a maximum of $1,080 to 10 million people. We should expect an increase in the petroleum resource rent tax (PRRT). When Chalmers highlights "pressures on budgets from an ageing population" and "equality and opportunity", he wants a tax reform agenda.

For hints on where he may go, we can look at two recent speeches by his main adviser, Treasury Secretary Steven Kennedy. Speaking to the Economics Legislation Committee on 15 February 2023, Kennedy said:

"We expect fiscal challenges to persist over the medium term. Persistent deficits of around 2% of GDP are projected, with several payments growing faster than the economy. This includes interest on government debt, and growing expenditure on the NDIS, health, aged care, and defence. The projected structural deficit throughout the medium term makes the need for fiscal consolidation clear."

What is this Treasury-speak, fiscal consolidation? It is reducing government deficits and debts.

Then on 3 April 2023, Kennedy gave another speech, to the Policy Research Conference (yes, he enjoys a very exciting life!), where he said:

“This means the tax system should aim to treat individuals with similar economic capacity in the same way, raise and redistribute revenue at the least possible economic cost, and be simple to understand. Australia’s tax system is not always consistent with these principles. For example, it is easier to reduce tax on income from passive sources than it is for salary and wage income.”

Passive income include non-salary items such as rent, interest, dividends and capital gains. Kennedy has previously criticised techniques used in tax planning including trusts, companies and superannuation.

So Chalmers and Kennedy have much in common on the policy front, and they are the two big guns on 9 May 2023. Some type of transfer from investors to salary earners seems likely, and perhaps some changes to the Stage 3 taxes.

With the Government wanting fewer large balances in super, and pushing retirees to spend their savings, there is little likelihood that the halving of the minimum pension percentage that has applied since 2019/20 (for four financial years to 2022/23) will continue for another year. This will be a shock to some couples with $1.7 million each in a super pension who recently turned 65, where their drawdown must increase from 2% ($34,000 each, total $68,000) to a whopping 5% ($85,000 each, total $170,000). That's a lot of money that cannot be recontributed to super. The percentage required drawdown rises to 9% from age 85 to 14% at age 95, although forced withdrawal at that age is probably doing the retiree a favour to avoid the 17% 'death tax'.

***

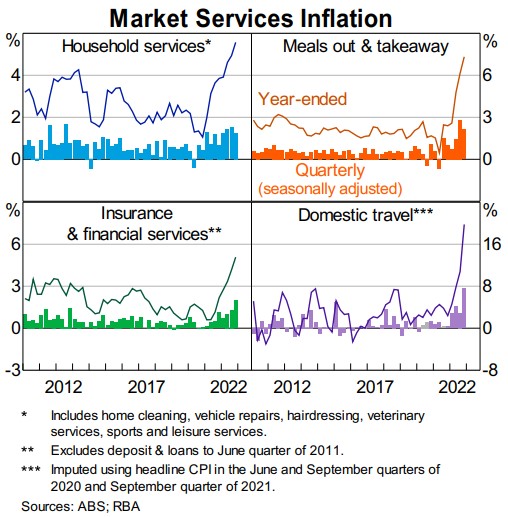

There are limitations to the value of personal or anecdotal evidence, especially as it may reflect idiosyncratic preferences rather than general experience. But one aspect of inflation that looks like a vast understatement is 'meals out and takeaway'. It is gobsmacking how quickly prices are rising in cafes and restaurants, far above the official statistics in my experience. I wonder how the numbers allow for 300% markups on wine, the offer of sparkling water without saying it costs $7.50 each, upselling of $6 bread and smaller portions (so-called 'shrinkflation'). Does the statistician recognise the increasing trend to charging for vegetables (the world's most expensive Brussels sprouts) separately which adds 25% to the cost of a main meal? The 15% surcharge last Saturday night for a public holiday came as an expensive surprise when we all thought the Easter holiday days were Friday and Monday.

I hope Governor Philip Lowe is not dining out much because if he sees these prices at packed restaurants, he will think the official numbers are underdone and most people have not received the message to manage their spending to control inflation. At least the travel numbers seem to reflect reality better.

I am far from alone in wondering how takeaway and restaurant food suddenly became so expensive.

If there is one person in Australia who understands the consumer, it is Solomon Lew, Chairman, Premier Investments (owner of the Smiggle, Peter Alexander, Just Jeans and Portmans stores, among others) and in recently announcing good trading results, he said:

“I think the consumer is somewhat out of control…They’re used to shopping, they’ve got used to going out to restaurants, got used to spending money…The aspirational demand for these products is just still out of control.”

So stop spending if you want interest rates to come down.

***

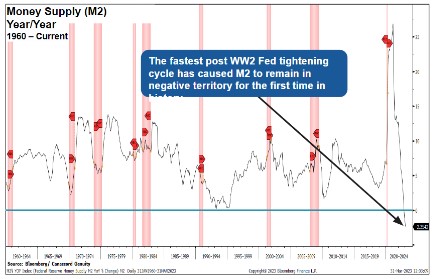

These days, most economists and central bankers pay less attention to money supply (the sum of all of the currency and other liquid assets in an economy, including cash in circulation and all short-term bank deposits) than 30 years ago. The chart below shows the extraordinary rise in M2 money supply in 2020 which monetarists argue caused the current inflation, and now, a fall to negative in the US for the first time in a rapid tightening of policy.

Credit Outlook, M2 (Money Supply) Historically Negative.

We look at the latest update from Professor Tim Congdon who warned us in 2020 that central bank policies would cause inflation, and now he explains the consequences of money supply contracting. It's not good.

Jamie Dimon is the world's most influential commercial banker, and he recently published his annual letter to JP Morgan shareholders. We summarise his major messages, and while the US economy is in decent shape at the moment, he explains why this time is different.

These warnings are backed up by the International Monetary Fund (IMF), which this week predicted declining global growth, and in Australia, federal and state deficits until at least 2030. The government interest cost will consume 1.8% of GDP by 2028. In response, Jim Chalmers said:

“All of these costs are putting pressure on the Budget. There is a structural problem and we need to deal with it.”

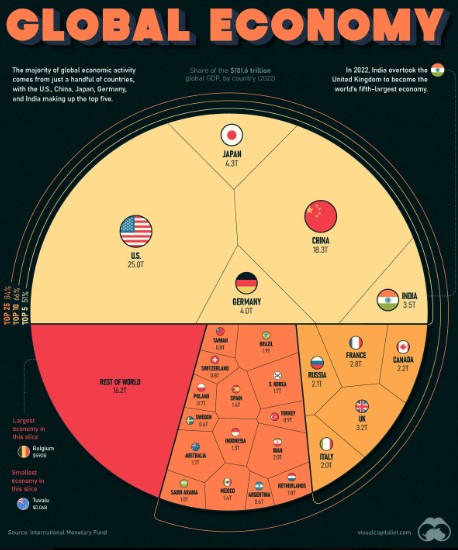

For anyone wondering why analysts focus so much on the US, this chart shows of the US$100 trillion in global GDP (according to the IMF in 2022), the US contributes 25%. Find Australia and see why we only make the news in the US when a shark bites someone or arranges a golf tournament.

Graham Hand

Also in this week's edition ...

Fund managers like to talk about the stocks they own and why. Yet, as Dr Justin Koonin and the team at Allan Gray point out, outperforming over the long term doesn't solely depend on the stocks you pick. It also depends on how you weight those stocks in your portfolio. Justin looks at how to construct a successful stock portfolio.

Is there an advantage in being a member of a large super fund? Yes and no, say Geoff Warren and Scott Lawrence. Their research suggests that it's not size that matters as much as how it's used. If a large fund can leverage the advantages of size, then members can be better off. But operating effectively at scale faces many challenges. In the end, what matters most is how well management executes.

Forget that conservative 4% withdrawal rule. Retirees can safely remove 15% of their portfolio’s assets every year, for life. Morningstar's John Rekenthaler uses this somewhat tongue-in-cheek statement to highlight a key point: that when evaluating investment yields or retiree-withdrawal rates, consider not just the numerator’s percentage, but also the denominator’s effect. That is, it's not only the 4% that matters, but 4% of what.

An important part of anyone’s life is deciding what happens to their assets when they die, or in the latter time of their living. We have received a few requests to write more about estate planning, including helping children into their own home. As an interim step, we are reprising an article by Chris Cuffe, who says he is surprised how little thought many people put into a lasting legacy. Chris goes through the basics of estate planning and how to create a fund for future generations.

Is the boom in ETFs set to slow down? James Gruber reports that a new survey of global ETF executives suggests industry growth is unlikely to taper any time soon. Investors here can expect vast array of new products in alternative strategies, cryptocurrency, ESG and active ETFs.

In the weekend update by Morningstar, Sarah Dowling looks at 11 ASX stocks offering great value right now, while Josh Peach examines the Australian tech companies set to benefit from a current cost-cutting wave.

Lastly, in this week's whitepaper, Capital Group analyses the likely impact of artificial intelligence and the opportunities arising for investors.

***

Weekend market update

On Friday in the US, a late bounce helped stocks erase the bulk of intraday losses as the S&P 500 finished up 25 basis points to settle higher by 1.4% for the week, while Treasurys sold off with the two-year note rising 12 basis points to 4.08% and the long bond rising to 3.74% from 3.69% Thursday. Gold pulled back to $2,018 an ounce, WTI crude edged higher towards $83 a barrel and the VIX logged a fresh 52-week low near 17.

From AAP Netdesk:

The Australian stock market lifted for a third straight week at the close. The benchmark S&P/ASX200 index on Friday closed up 37.5 points, or 0.5%, to 7,361.6, while the All Ordinaries finished 39.7 points higher, or 0.5%, to 7,560.4.

Local shares ended the week up 2%. The three-week winning streak follows seven consecutive weeks of losses over February and March.

Nine of the 11 official ASX sectors closed higher on Friday, with the mining and finance sectors showing most improvement.

Minerals company IGO Limited rose 5.3% to $13.43, supercharged after the miner and billionaire mining magnate Andrew Forrest's Wyloo Metals secured land from the West Australian government to develop a facility that produces precursor materials for batteries. Fortescue Metals, which Mr Forrest leads, was also riding a wave of optimism after closing the day up 1.3%.

Gold stocks shined with Silver Lake Resources a standout, gaining 6%, while Regis Resources rose 4.3%. Bellevue Gold will enter Australia's list of 200 biggest companies following BHP's acquisition of South Australian miner OZ Minerals on Thursday. The WA-based company's shares rose on the news, finishing up 1.7% to $1.51.

The major banks all finished higher with NAB increasing by 1.2%. CBA and ANZ both recorded gains of 0.9% while Westpac finished the week up 0.7%.

The energy sector closed out the session increasing by 0.5%. However, Karoon Energy's share price sank by 5.4% to $2.26 after the oil and gas exploration company was forced to extend a suspension of production at its Bauna oil well off the coast of Brazil, resulting in lower production and increased costs.

Healthcare and property industries fell into the negative at the close. Healthcare benefits from a stronger US dollar and a weaker Australian dollar, which is the opposite of the current situation.

Investors saw the best in clothing retailer Best & Less announcing Erica Berchtold, the soon-to-be former boss of online fashion retailer The Iconic, would assume the role of chief executive in September. The bargain boutique's share price rose by 2% to $2.06 at the close.

From Shane Oliver, AMP:

Global share markets had a strong week helped by a further fall in US inflation adding to expectations that the Fed is at or close to the top. For the week US shares rose 0.8%, Eurozone shares gained 1.7%, Japanese shares rose 3.5% but Chinese shares fell 0.8%. The positive global lead helped boost Australian shares which rose 2% for the week with gains led by material, IT, property and energy stocks. Bond yields rose as did oil, metal and iron ore prices. The “risk on” tone also saw the $A rise as the $US continued to fall.

Inflation pressures are continuing to recede. This was evident in a further fall in US inflation and even Indian inflation falling to a 15-month low. US inflation fell to 5%yoy in March with a sharp slowing in annual energy and goods price inflation leaving it well down from its high of 9.1% in mid last year.

While US core (ie ex food and energy) inflation remains sticky at 5.6%yoy due to high services inflation, core services inflation excluding shelter (a key focus of Fed Chair Powell) is starting to slow and shelter (or rent) inflation is also starting to slow with advertised rents pointing to a further slowdown ahead.

Yield curves continuing to point to a high risk of US recession – and that the Fed has probably done enough. A sharp fall in bond yields since February and still rising short term interest rates has seen US yield curves invert further (ie long term rates fall further below short term rates). Even the near term yield curve – which some at the Fed appear to prefer – as proxied by the gap between the 2 year bond yield and the Fed Funds rate - has now inverted. Over the last 50 years all US recessions have been preceded by inverted yield curves as is the case now – but the lag can be up to 18 months and it can give false signals.

In Australia, the yield curve has also now inverted warning of a rising risk of recession - but its track record in signalling recession is poor. The decline in long term rates below the cash rate is signalling though that the money market expects that the RBA has probably also done enough to control inflation.

Latest updates

PDF version of Firstlinks Newsletter

ASX Listed Bond and Hybrid rate sheet from NAB/nabtrade

Listed Investment Company (LIC) Indicative NTA Report from Bell Potter

Plus updates and announcements on the Sponsor Noticeboard on our website