There’s a confluence of events boosting Australian property prices, especially in Sydney, but none is more pervasive than the Fear Of Missing Out (FOMO). All investment markets are driven by sentiment, and when it’s impossible to pick up a newspaper without the latest story on 85% auction clearance rates and smashing of reserve prices, potential buyers change their mindset. They may have trudged from one open house to another in 2012, waiting for the no-compromise property, but now they are jumping in before prices rise further. According to RP Data-Rismark, prices in Sydney were up 5.2% in the September 2013 quarter and 10% since the start of the year, multiple times the rise in average weekly earnings.

A common technique used to promote properties is to quote the gross yield. Purchase price $700,000, rent $700 a week, that’s $36,400 a year or 5.2%. Even better, many inner-city apartments can become part of a short-term apartment letting scheme, like a long-stay hotel. Room rates might be as high as $300 a night during a major event, $200 at other times. That’s double the weekly rent of a lease. It’s a no-brainer.

It’s only when the off-the-plan property settles a year later, or time comes to select an agent and a decent tenant, that many investors face a harsh reality check. The costs are always greater than expected.

The confluence which is creating the competitive forces behind FOMO includes:

- various first-home buyer schemes and stamp duty exemptions

- investors moving money out of cash and term deposits into the growth asset class they believe they understand and is not volatile

- Asian buyers, especially Chinese who are restricted in owning property in their own country. Asians love property and Australia is seen as more stable than Europe or the United States. They often have children studying here

- SMSFs are the new players, and although the amounts are not high in absolute terms (only about 3% of SMSF assets are residential property and three-quarters of property assets are commercial), it’s a new competitive influence

- other residential property investors (local non-super) who have regained confidence at a time when unemployment remains low and financing has never been cheaper.

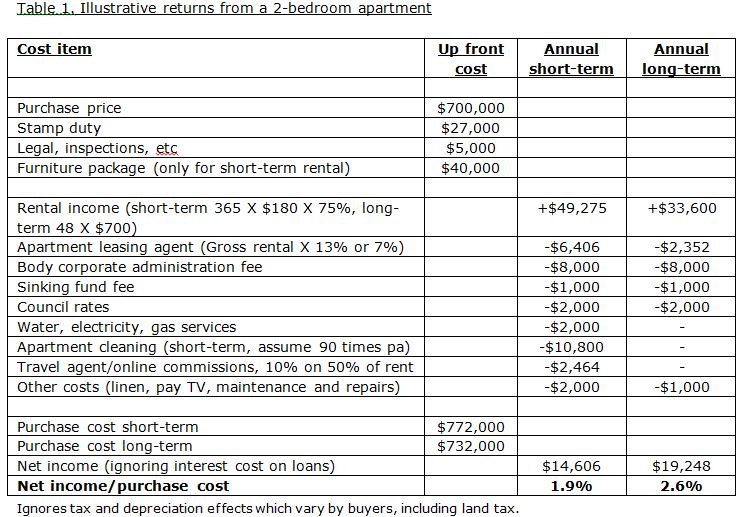

But let’s take a look at the harsh reality check facing many of these exuberant buyers, considering the costs of purchase and owning an apartment with either short-term or long-term rents:

- Stamp duty. Stamp duty varies from state to state at about 3-4%. On a $700,000 property in New South Wales, stamp duty is about $27,000. Imagine transaction costs of that amount in the share market. The efficient allocation of equity capital and efficient trading would be compromised.

- Legal costs, loan establishment fees, valuations, building inspections, etc. Let’s call it $5,000.

- Mandatory furniture package for short-term rentals. Need to set a high standard for someone paying up to $300 a night, so full package for a 2 bedroom serviced apartment say $40,000.

- Apartment leasing agent. Between 6% and 15% of gross income depending on the type of leasing plan.

- Body corporate administration fees. These are often deliberately understated during the selling period, but there are four killers to watch for: 24 hour concierge, swimming pools, lifts and gymnasiums. Then there’s gardening, fire services, cleaning. A decent building and apartment will cost at least $2,000 a quarter to maintain all these services. No point paying a million for an apartment and not maintaining the building.

- Body corporate sinking fund. Again, depends on what is agreed by the body corporate but set for future major capital expenditures, such as repairs or repainting the entire building. Say another $1,000 per annum.

- Council rates. Although charged on the ‘unimproved capital value’ of an apartment rather than the land value of a house, it could easily be $2,000 a year on a $700,000 apartment.

- Water, electricity, gas. Usually paid by the tenant on a longer lease but by the owner in a short term apartment scheme, rising rapidly and maybe another $2,000 a year.

- Vacancy. Long-term leases allow 4 weeks a year, short-term depends on the success of the managing agent or apartment scheme operator. May need to discount rates to compete, especially in winter. Assume short-term occupancy is healthy at 75%.

- Apartment cleaning. A 2-bedroom apartment leased for a few days might cost $120 to clean, giving an annual cleaning bill of over $10,000 (assuming apartment rented for 270 nights a year for 3 nights each time, that’s 90 cleans). There’s no choice to clean it yourself, it’s all part of the apartment scheme.

- Travel agent's commission. Short terms pay online services such as wotif.com 10% of the rental, and similar for travel agents. Assume paid on half of rentals.

- Replacement of furniture and equipment. The short-term agent will say that the apartment looks tired and needs a complete refit. Not all tenants are neat, tidy and careful. Some will have raucous parties, kick a door, smash a vase. After a few years, the sofa will be disgusting, the carpet filthy and the mattress stuffed. Expect to replace the furniture at least every five years, and probably the entire kitchen and bathroom every 10 to 15 years. Everything in the apartment will need replacing regularly, plus painting and air conditioning. Cost per annum, say $10,000 (ignored in the table below to avoid double-counting with original cost).

- All the other stuff. Where do we stop! There’s a linen fee, pay TV, PABX, credit card fees, advertising, insurance and postage fee. The agent charges $20 to replace a light bulb, $15 to adjust the TV, $200 to fix the dishwasher, using tradesmen who have a far closer relationship with the agent or building manager than the owner. The apartment will be better maintained than the owner’s home. Call it $2,000 a year on short-term leasing.

At this point, faced with all these costs, administration and paperwork, the apartment owner draws on two sources of comfort: tax savings and capital gains.

First, tax savings. If the property is negatively geared, there is a deduction against other assessable income. Other costs make the tax deduction even higher. What many owners fail to recognise is negative gearing is a polite way of saying ‘loss’. A loss is still a loss, even if tax reduces the size of it. Furthermore, tax is paid in an SMSF at only 15% in accumulation stage or nil in pension phase, so the tax savings are far less than a high marginal tax-paying individual.

Second, capital gain. It is irrelevant to someone buying today that prices are up 10% this year. All that matters is the future. Buy an apartment for $700,000 and sell it for $750,000 a year later and there won’t be much left over to pay for all the hassle. It costs most of the gain to buy, finance, repair and keep it. It’s easy to believe that property prices are one-way traffic, but Sydney has only just recovered in real terms the prices from 2004. That’s almost a decade with no real growth. It’s as convincing to make a case for prices falling in years to come – rising interest rates, increasing unemployment, historically high price-to-rent ratios – as it is to bank on capital gains.

Apartment

Of course, any of these assumptions can be varied (including using lower rents and higher costs), but the net rental income from residential investment, ignoring interest costs, is around 2% to 2.5%. Rents do rise over time, but not much in real terms, and so do costs.

There’s a decent chance the day the apartment is bought, when the thrill of owning a property is matched by dreams of income and capital gains, is the highlight of the investment. After the calculations, paperwork and administration are done, taking phone calls from agents saying the toilet needs fixing quickly becomes tiresome.

Like any investment, residential property must be the right asset bought at the right price and the right time, not anywhere based on the need to get into the market quickly due to FOMO. It might be that the recent price rises have already delivered the best returns for some time.