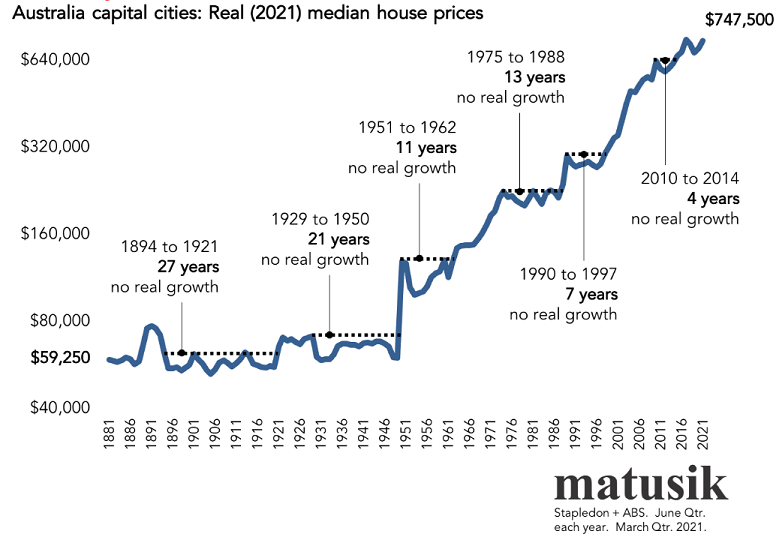

Australians believed house prices would never go down, until they did last year. Yet the downturn has been mild so far compared with those of the past. For instance, Melbourne house prices went down 51% in real terms (prices minus inflation) in the 1890s. Real prices nationally were flat for 60 years until 1950. Prices went down more than 20% in key cities during the 1980s.

History shows the housing market has been a story of boom and bust. Today, we look at previous downturns: what caused them, how they played out and what we can learn from them.

As Mark Twain once said, “History never repeats itself, but it does often rhyme.”

The 1890s collapse

The 1890s witnessed Australia’s worst ever house price decline. Not only did Melbourne’s prices fall more than 50% in real terms, but Sydney’s also fell 36%. House prices then went nowhere for 60 years. In other words, an adult at that time often didn’t see a time when property was a good investment.

The boom which preceded the bust was as equally spectacular. It started in the 1850s and 1860s with the gold rush. And the mining boom continued into the 1880s and gave birth to the likes of BHP – originally named The Broken Hill Proprietary Company, operating a silver and lead mine in Broken Hill – and Rio Tinto – which was established overseas.

The mining upturn was accompanied by a flourishing agricultural sector, especially the rapid growth of the wool sector.

The economic opportunities from the boom attracted a large inflow of immigrants. Australia’s population went up 8x from 400,000 to 3.2 million. Melbourne population grew 16x from 30,000 in 1851 to 485,000 in 1890, or 7.5% per annum!

Unsurprisingly, housing demand took off during the period and prices moved up sharply. A house construction and lending boom soon followed. Yet by 1885, there was a housing surplus, and the market started to falter. Construction reaccelerated once more before falling and 1889 marked the peak in prices.

Banks helped propel the property upturn. The 1870s and 1880s also witnessed the proliferation of non-bank institutions such as building societies, which weren’t shy about lending freely to property developers.

Overseas investors becoming concerned about their Australian investments. A crisis at Barings Bank in London in 1890, although focused on Argentina, led to a reassessment of Australian holdings and withdrawal of funds.

This, and the property crash, caused a banking crisis. The Bank of Van Diemen’s Land was the first major bank to fail in 1891, and 13 others followed. Consequently, the eastern colonies suffered a severe economic depression in 1890-1891.

World War One

The next property downturn was milder and briefer. In real terms, prices fell but not by much. World War One impacted both the supply and demand for housing. Demand was hit by soldiers going off to fight in the war as well as a slowdown in immigration. Also, investor demand fell as rents went down, partly due to government measures to protect soldiers from any increase in rents. Because demand fell, supply cuts followed.

Prices and rents didn’t really pick up until 1920 as Australia worked through the devastation wrought by the war. Immigration started to increase again and unbeknown to people at the time, it was to be the start of the 1920s economic boom.

The Great Depression

The boom centred around agriculture. Wool had been Australia’s primary export to this point, but new goods such as wheat, dairy, and other produce were introduced. Soldiers returning from the war were resettled on farms and more than 200,000 government-sponsored British immigrants arrived, many heading to country towns.

As European countries started to recover from the war, the US, Argentina, and Canada saw the opportunity for increased agricultural demand. This led to a global oversupply in two of Australia’s major exports: wheat and sheep.

Meanwhile, federal and state governments were borrowing freely from overseas institutions throughout the 1920s. They used the money on major public infrastructure works. But, when commodity prices started to decline in 1927, the overseas money dried up.

As commodities dipped and overseas economies and stock markets tanked in 1929, Australia experienced its largest-ever economic decline. Income dropped by a third and unemployment peaked at 32% in 1932.

Housing during the Great Depression fared much better than the 1890s. Yes, nominal prices fell more than 25% from peak levels but due to the substantial deflation at that time, real price declines were far less. From the highs of 1929, Sydney and Melbourne property prices fell 11% and 13% in real terms to their respective lows in 1932 and 1931 (compared with the 36% and 51% falls of the 1890s) and they recovered most of those declines by 1939.

The reasons why housing didn’t fall further were three-fold:

- The prior boom of the 1920s was relatively mild.

- Rents didn’t decrease as heavily as in the 1890s.

- Bank balance sheets were in better shape.

World War Two

Governments introduced house and rental price controls in 1942. With significant inflation due to the war, it left property prices at ludicrously low levels by the time price controls were lifted in 1949. And when the controls were removed, prices went gangbusters. In Sydney, they went up 77% in about 12 months.

Prices peaked in real terms in 1950 and then fell by 25% by 1953. The main reason for the drop was the preceding overshoot in prices when price controls were lifted.

Interestingly, the lifting of price controls coincided with a transformation in the structure of the housing market. The rental share of houses in capital cities declined from 55% of the market in 1947, to 20% in 1961. This can be attributed to recovery from the Second World War, a huge influx of immigrants from Europe, a surge in economic growth in the 1950s and the major infrastructure projects initiated by Labor governments after the war.

It was during this period that the ‘Australian dream’ of owning a home took shape.

The 1974 downturn

The property boom of the 1960s and early 70s was the result of many factors:

- The natural economic upswing that took place after World War Two not only in Australia but overseas.

- The mining boom during the 1960s.

- The large population increase through increased immigration.

- Higher density developments to cater for more people.

- The expansion of cities and infrastructure to help house more people.

- The increasing sophistication of capital markets and the beginnings of Sydney as an international financial centre.

- The housing boom was aided by a lending boom. Banks and non-banks joined in the party.

By 1974, Sydney residential prices were up 116% from their 1950 peak in real terms while Melbourne’s was up 47%. Sydney fared better due primarily to a sharp increase in fringe land prices.

From their peaks, Sydney and Melbourne prices fell 18% and 24% respectively in real terms. Whereas real price falls in the 1890s and 1930s translated into nominal price falls, the high inflation that epitomised the 1970s cushioned the fall for the property market and protected the banking system.

Yet, property prices didn’t reach 1974 levels in real terms until 1988, 14 years later.

The 1990s recession we had to have

The seeds of the 1990s housing downturn were multifaceted. The early 80s brought a mini-mining boom that turned into an entrepreneurial boom, with colourful personalities including John Spalvins, Robert Holmes a Court, Alan Bond, John Elliott, and Christopher Skase splurging money lent by deregulated banks.

This was against a backdrop of significant economic reform from the then Labor government, including the floating of the Australian dollar, removal of limits on the interest rates that could be paid on deposits and charged for loans, and introduction of competition from foreign banks.

The increase in access to credit led to a late 1980s construction and lending boom which turned into a bad bank debt crisis in 1990-1991. Many banks collapsed including the State Bank of Victoria, the State Bank of South Australia, the Teachers Credit Union of Western Australia, and the Pyramid Building Society in Victoria.

During the recession, GDP fell by 1.7% and the unemployment rate rose to 10.8%.

Despite this, the downturn in residential housing was mild. From peak to trough, prices decreased nationally by just 8% in real terms. The Melbourne’s market fared worse, with a drop of 19%, thanks to a string of banking failures and subsequent job losses.

It was the commercial property market that suffered more. For instance, Sydney office prices declined 40%. It was problems in commercial property that led to banking troubles and recession.

The 2022-2023 bust

The causes for Australia’s current downturn may be simpler than previous downturns. The Reserve Bank of Australia and other central banks kept interest rates at levels well below inflation rates for most of the past 20 years. Unsurprisingly, it fuelled booms in almost everything, including real estate.

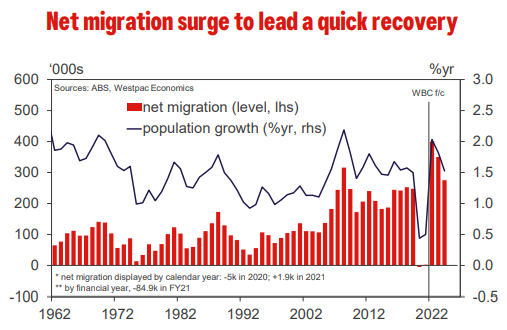

In Australia, the housing upturn was helped by significant population growth pre-Covid, strong labour markets, and supply shortages driven by government costs/taxes/inaction.

In the three years to the end of 2021, median house prices surged by 43% in Sydney, Brisbane, and Canberra, 41% in Melbourne, and 62% in Hobart. The boom in house prices ended with the rate hikes in 2022.

Even after price falls of 10% in 2022, nominal prices remain well above where they were before the boom began.

Where to from here?

If there’s one lesson from history, it’s that the larger the real estate boom, the larger the likely bust. Given the extraordinary house price rises that took place up to 2021, that’s cause for concern.

Yet each period is different, and our current one has positive and negative features for the property outlook.

The positives:

High population growth and favourable demographics. Unlike many other Western countries, Australia enjoys strong population growth driven mainly by immigration. Net migration totalled more than 400,000 people last year, while this year another 350,000 is expected – both huge numbers. Our demographics are also favourable for the housing market with fewer people per household going forward.

Favourable tax treatment. Tax breaks include negative gearing on investment properties, exemptions from capital gains, and means tests on owner-occupied homes. These should remain in the short-term, though given the size of these tax breaks, governments will eventually have to trim them.

Supply constraints. Driven primarily by people who don’t want further development in their neighbourhoods and the councils that pander to these residents.

The negatives:

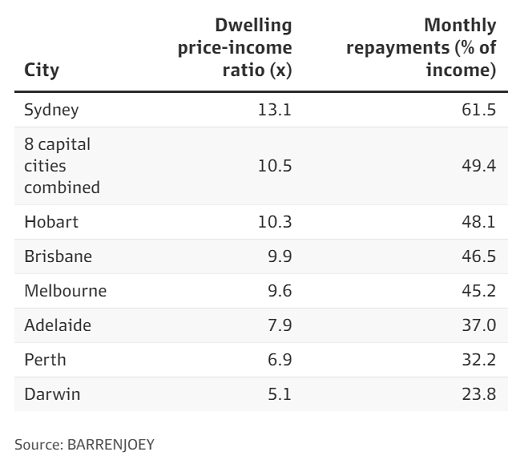

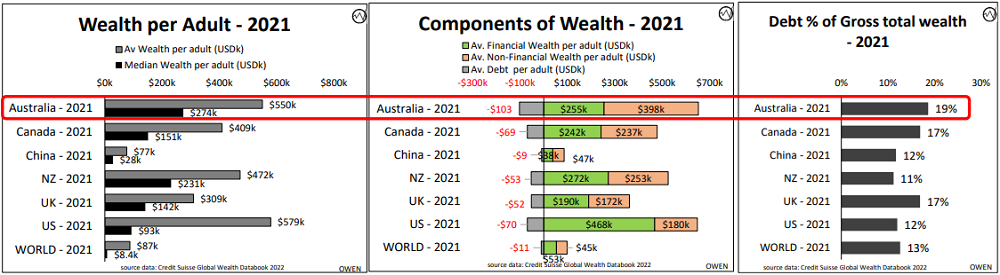

High household debt. Australians are the wealthiest in the world, and 72% of that wealth is in housing. We’re also the most indebted, in absolute and debt-to-asset terms. Mortgage monthly repayments has risen to 50% of income, a high number that’s likely to squeeze many households.

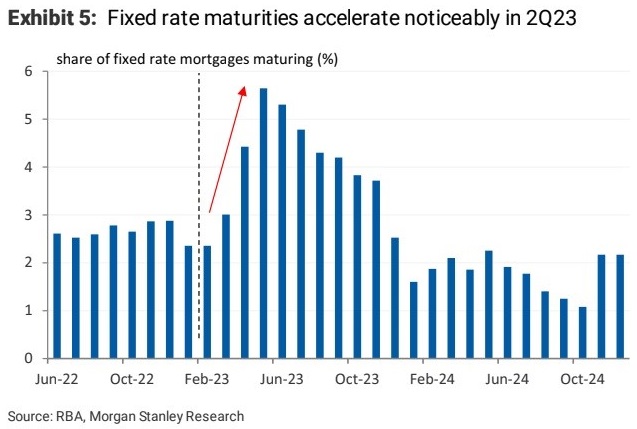

High percentage of variable rate debt. Unlike in the US where people are principally on fixed-rate loans, the bulk of loans in Australian are variable rate. That means any change in the cash rate immediately impacts people here. There’s also close to 900,000 loans totalling $350 billion switching from fixed rate to variable rate this year, and that’ll result in much higher rates for these loans.

The large number of investors who own residential property. Out of around 10.8 million residential homes, investors own 3.25 million, or about 30% of the total.

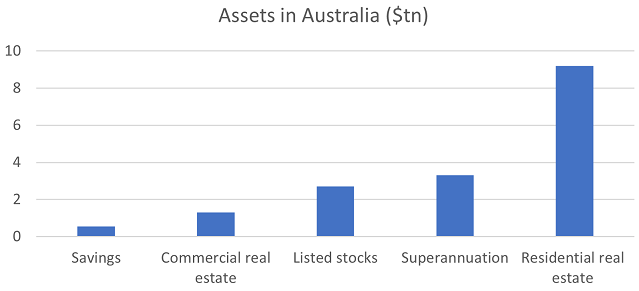

Residential property’s size makes it too big to fail. The total value of residential property at $9.3 trillion dwarfs our annual GDP of $1.55 trillion. Crash housing and it’ll crash the economy.

Source: Corelogic, Finder

Valuations. With 10-year government bond yields at 3.65% and mortgage rates close to 6%, current nationwide rental yields of 3% for houses and 4.5% for apartments look decidedly unattractive. For them to offer better value, rents will have to rise a lot, or prices will have to decline, or a combination of both.

James Gruber is an Assistant Editor at Firstlinks and Morningstar.

References: The history in this article has been sourced from the following: Nigel Stapleton’s academic paper, ‘A History of House Prices in Australia, 1880-2010’, various monthly reports from Stanford Brown’s Ashley Owen, and John Vander Have’s UNSW graduate paper, ‘The 1974 Collapse of the Property Market in Sydney’, and Corelogic reports on the 2022 downturn.