Economists are not best placed to decide if we are in a stock market bubble. But as we look to the future of artificial intelligence’s (AI) impact on global economies, we see two potential scenarios: an ‘AI Boom’, where AI is the real deal and is rapidly adopted; and an ‘AI Bust’, where a stock market bubble bursts. Read on for a summary of our research, or download the full paper above or via this link.

Two scenarios, one beginning

Both scenarios are based on our key assumptions that the solid macroeconomic backdrop, coupled with the sizeable investment plans of the hyperscalers – the big cloud computing companies – will see continued capital expenditure (capex) and a rising equity market performance for much of 2026.

We then assume a key moment late in the year when markets begin to question the ability of tech companies to deliver on the hype. Will the technology be monetised sufficiently to deliver a return on investment? At this fork in the road, our scenarios diverge.

In the ‘AI Bust’ scenario the stock market bubble bursts and tech companies pull back from rapid investment, which has a negative impact on the broader economy.

By contrast, in the ‘AI Boom’, clear evidence emerges from the market wobble that AI technologies – not only large language models (LLMs), but also autonomous robotics, vehicles and more – are shown to be transformative and profitable.

This is then assumed to spur rapid adoption of the technology that could see new market leaders emerge.

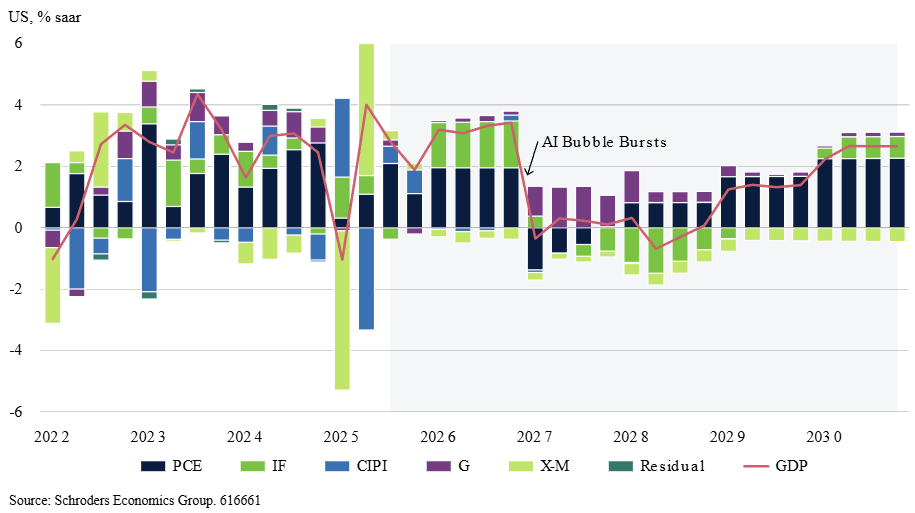

AI Bust

The many past instances of the bursting of historic market bubbles mean we can be more confident about the macroeconomic implications of this scenario.

We assume the market collapse would have an immediate, negative effect on private sector activity. As it becomes clear that tech companies will not be able to monetise AI investment, spending is shelved. We then assume a two-year investment recession like that seen in the aftermath of the dot.com bubble in the early 2000s.

Falling stock prices and rising unemployment would have a negative impact on sentiment and spending. This would be enough to tip the US into a mild recession.

Rising unemployment and softer demand would relieve capacity constraints in the US economy and allow the Fed to cut interest rates to below neutral.

This, coupled with some fiscal stimulus, would set the scene for a cyclical, consumer-led recovery through late-2028 onwards.

In this environment, equities would begin to perform well again, but with more breadth and different market leaders.

AI Bust - Capex drops, with negative impacts on sentiment and spending

Note: PCE = Personal Consumption Expenditures, IF = business investment, CIPI = change in private inventories, G = government spending, X-M = net exports

AI Boom

The AI Boom scenario is deliberately assumed to be extreme in order to tease out the long-term implications of a rapid, ‘third industrial revolution’ which unfolds over a matter of months rather than years or decades.

We have assumed that after a market wobble in late-2026, there is some pause in tech capex as the winners and losers of the AI arms race are thrashed out. After that, our key assumption is of an exponential ramp-up of capex as firms rush to roll out AI infrastructure and services as it becomes clear that AI is deeply transformative.

This is assumed to support robust US GDP growth.

However, in such a scenario where robotics and autonomous vehicles, amongst other technologies, begin to displace workers, the outlook for consumption is less clear cut.

We have assumed the AI Boom sees US productivity growth climb to the rates seen prior to the dot.com bubble and stay there – around 3.5% per year.

By assuming that both population growth and participation rates remain the same, such strong productivity would imply an increase in unemployment.

US productivity boom results in rising unemployment

Twin-speed growth and inflation

It is also easy to construct a twin-speed story for US inflation in such a scenario.

Rising unemployment and pressure on incomes and consumer spending all sound deflationary – certainly for areas such as housing and core services. At the same time, the displacement of workers could bring down the cost of other service sectors.

However, the scramble to rapidly adopt transformative AI would likely cause strains on various areas of the economy. If tech firms struggled to keep up with strong demand, it is fair to assume there would be an inflationary impact in the goods sector.

There is also a lot of focus on the energy demands AI is likely to trigger through power-hungry data centres. Around half of US electricity is generated using natural gas, and rising demand could see prices rise.

Given the importance of natural gas to fertiliser production, it is feasible this could also begin to put upward pressure on food prices.

Tricky environment for policymakers

Ultimately, rising lay-offs and falling inflation would pave the way for much lower interest rates.

The prospect of jobless growth could also have profound implications for the US public finances.

Around three-quarters of federal revenues come from the taxation of labour whereas only about one-quarter comes from corporations. On the other side of the ledger, a large portion of federal spending is on welfare.

The implication is that the US – and other governments around the world – would need to raise more tax from corporations and perhaps totally overhaul tax and spending frameworks.

But finally, to take a step back, the most obvious question to come out of this scenario is whether governments would ever allow such unfettered adoption of AI.

From an investor’s point of view, monitoring these developments is critical.

Where potential AI scenarios are as divergent as igniting a boom or triggering a bust, complacency must be among the bigger risks.

David Rees is Head of Global Economics at Schroders, a sponsor of Firstlinks. This article does not contain and should not be taken as containing any financial product advice or financial product recommendations. It does not take into consideration your personal objectives, financial situation or needs.

For more articles and papers from Schroders, click here.